Launching a payment franchise is one of the most profitable ways to enter the fast-growing fintech and merchant services industry.

So whether you are an entrepreneur, sales agency, or existing business owners who are looking to diversify revenue, partnering with Ace Merchant Processing gives you everything you need to start and scale your own merchant services franchise spanning from payment terminals and gateways to onboarding tools, real-time reporting and 24/7 support.

Through this guide, you will learn how to build a payment franchise step-by-step, from setting up your legal structure and signing your partnership agreement to onboarding merchants, managing chargebacks, and creating a predictable monthly residual income stream.

We will cover how Ace Merchant Processing helps franchise partners handle card payments, eCommerce transactions, and mobile wallet integrations across multiple verticals such as retail, restaurants, salons, healthcare, nonprofits, and more.

Unlike traditional reselling, a payment processing franchise that gives you ownership of merchant relationships , recurring transaction revenue, and brand equity in your local market.

This guide walks you through every stage such as planning, pricing, operations, marketing, and scaling while highlighting real examples and key metrics that drive return of investment.

If your goal is to build a profitable payment franchise with predictable income, low churn, and strong brand credibility, this step-by-step roadmap will show you exactly how to start, grow, and scale with Ace.

Also Read: What is Payment Processing Software

Why Build a Payment Franchise Now?

The payments industry is evolving faster than ever, creating a massive opportunity for entrepreneurs to build long-term, predictable revenue. A payment franchise with Ace Merchant Processing allows you to tap into one of the most resilient business models in fintech recurring revenue backed by real transaction volume.

Every time a merchant processes a card payment, you earn a small percentage through interchange and markup, creating ongoing monthly residuals which scale with your portfolio. This steady income grows as you onboard more merchants, turning each client into a reliable revenue stream.

Customer retention is another major advantage. Once payments are set up on a POS terminal or payment gateways, merchants rarely switch providers especially if the service is fast, secure, and transparent. That makes the payment franchise model one of the most stable in financial services.

Beyond transactions, payments open doors to cross-sell opportunities like POS software, gift cards, loyalty programs, business loans, and e-commerce integrations. These add-ons increase lifetime value while strengthening merchant relationships.

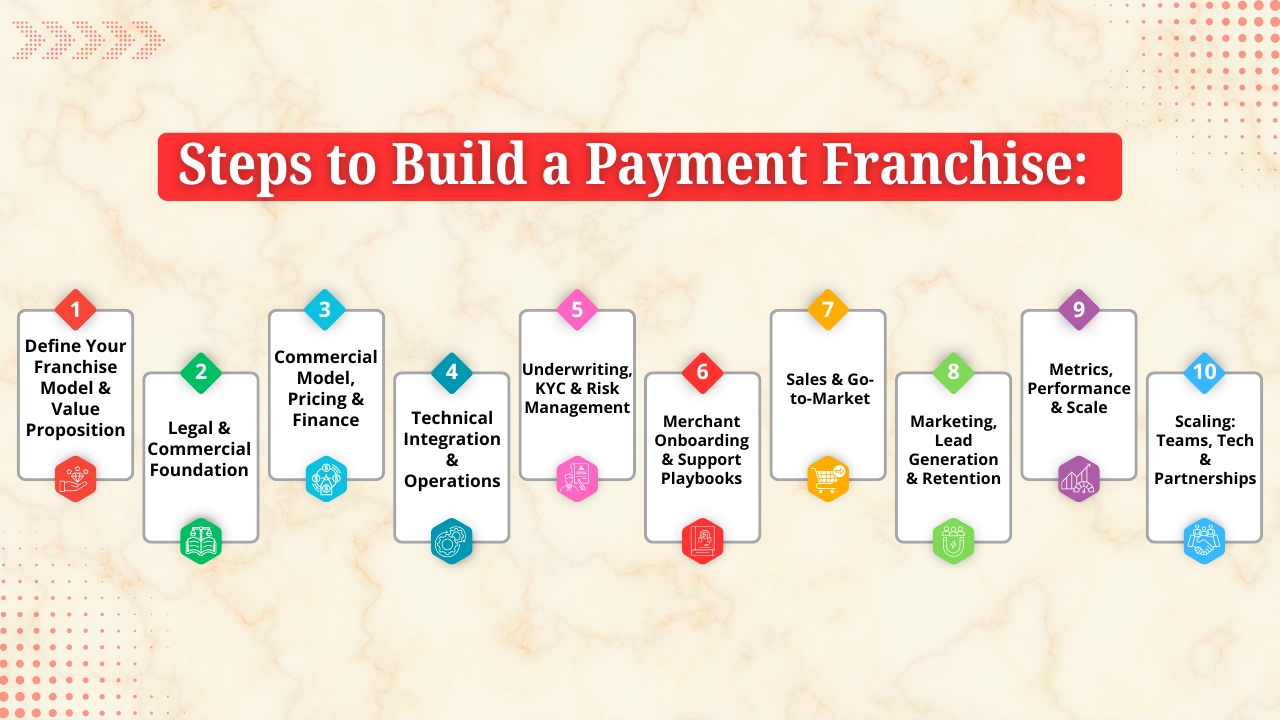

Steps to Build a Payment Franchise:

Step 1. Define Your Franchise Model & Value Proposition

Before you begin contracts or spreadsheets, clarify what type of payment franchise you want to run. This choice defines your margins, workload, and growth path.

1. Referral (Finder) Model:

You focus on lead generation by referring merchants to Ace Merchant Processing in exchange for a finder’s fee. It’s ideal if you want to start with low overhead and minimal operational responsibility. You don’t manage onboarding or support, making it easy to scale volume quickly.

2. Agent / ISO Model:

In this model, you onboard merchants under your brand or sub-MID. You handle initial KYC, setup, and first-line support, earning residual income from every transaction. It offers higher margins and control but requires dedicated staff, compliance, and CRM systems.

3. Managed Payments Provider (VAR) Model:

You integrate payments into a software or vertical platform such as POS, booking, or donation systems. It delivers end-to-end value and strong merchant retention, making it the most scalable, high-return path once your infrastructure is in place.

4. Positioning & Differentiation:

Your value proposition should clearly communicate why merchants should choose you over larger, faceless processors. Craft a clear, specific promise that reflects both service quality and local trust.

This concrete, service-driven value proposition separates your franchise from generic online processors and highlights reliability, speed, and personal support.

Also Read: Top 5 Features Every Retailer Should Look for in Modern Payment Terminals

Step 2. Legal & Commercial Foundation

Setting up a strong legal and commercial foundation is crucial before you start signing merchants or earning commissions. Below is how to build a reliable framework step by step:

1. Choose the Right Legal Structure:

The first step is to form a registered business entity such as an LLC, Pvt Ltd, or equivalent depending on your country’s regulations. Incorporating your payment franchise separates your personal assets from business liabilities, enabling safer contracts and professional credibility.

It also simplifies banking, settlements, and tax filings. A formal structure allows you to open a business account for receiving merchant commissions, manage payroll for sales teams, and apply for any required permits or financing in the future.

2. Secure Contracts & Partner Approvals with Ace:

Your relationship with Ace Merchant Processing is formalized through a reseller or ISO partnership agreement.Your partner contract should define commission or residual structures (upfront versus lifetime), assign chargeback or fraud liability.

Set pricing floors and allow markups with clear merchant-ownership terms, detailed sub-merchant underwriting and your support scope, and spell out exit, termination, and data-ownership provisions.

Negotiate co-branding rights and access to Ace’s API or SFTP for settlements, reports, and merchant analytics. This will let you integrate real-time data into your CRM or dashboard.

3. Maintain Regulatory & Tax Compliance:

Compliance protects both your brand and your merchants. Register for GST or VAT or sales tax depending on your local jurisdiction. Familiarize yourself with financial compliance laws such as AML(anti-money laundering) and KYC(know your customer).

In most cases, Ace handles these at the processor level, but you may be required to collect and verify documents. If your business ever holds or routes customer funds(rare), you may need a money transmitter or PSP license. Otherwise, make sure all settlements flow directly to merchant accounts via Ace to stay compliant.

4. Insurance & Risk Mitigation:

Protect your franchise with targeted coverage such as general liability for accidental claims, professional indemnity(E&O) for onboarding or setup errors, and cyber insurance if you store or process PII or payment data.

Also,maintain contractual limits on liability for fraud and chargebacks to avoid unexpected losses. A sound legal and commercial setup ensures your franchise starts on a secure, compliant, and scalable foundation.

Also Read: Top Retail Payment Trends Every Business Should Know

Step 3— Commercial Model, Pricing & Finance:

Creating a solid commercial foundation is the key to running a profitable payment franchise. Your pricing, commission, and financial modeling strategy must balance competitiveness, sustainability, and scalability.

1. Pricing Components:

Your pricing structure determines both your appeal to merchants and your long-term profitability. Every transaction in your business model is built on three layers:

2. Interchange + network fees:

These are mandatory pass-through costs charged by card networks such as Visa, Mastercard, etc. and vary by card type, region, and risk category. They are non-negotiable but must be disclosed transparently.

3. Processor or acquirer fees:

These fees are set by your payment partner, such as Ace Merchant Processing, and may be either fixed or percentage-based. These cover authorization, settlement, and infrastructure.

4. Your markup/ service fee:

This is your profit margin and the only flexible part of the equation. It usually combines a small flat fee per transaction and a percentage markup or blended rate. Design transparent, easy-to-understand pricing bundles to build merchant trust. Avoid overly complex statements or hidden surcharges.

This clarity simplifies sales conversations, improves conversion rates, and reduces post-onboarding disputes. Transparency should always be part of your brand promise so merchants must know what they pay and why.

Use data from Ace’s backend or your CRM to track profitability by merchant type and adjust markups accordingly.

5. Commission & Residual Strategies:

Commissions encourage your sales force, agents, and referral partners to bring in new merchants and keep them active. Build an incentive structure that rewards both acquisition and retention.

6. Offer channel incentives:

A popular model is paying 50% of the first-month profit to the referrer or agent, followed by 20% recurring residuals for 12 months. This combination of upfront reward and long-term income encourages partners to sell actively and maintain relationships.

7. Implement tiered commissions:

Different industries require different levels of effort. Restaurants, hospitality, and healthcare setups often demand additional configuration or KYC steps. Reward those who handle these verticals with slightly higher commission percentages.

8. Build a reserve strategy for chargebacks:

Protect your franchise’s liquidity by holding back 1-3% of revenue for merchants with higher risk profiles. This safeguard ensures you are covered in case of fraud or disputes while maintaining stable payouts to agents.

Ultimately, your commission model should be scalable, transparent, and performance-driven. Use CRM or dashboard tools to automate tracking so partners always know their earnings and payout schedules.

9. Financial Modeling & Forecasting:

A successful payment franchise operates on clear forecasting. Create a 3-year profit and loss model that includes all fixed and variable costs to keep your business profitable as it grows. Key elements include:

10. Merchant Acquisition Cost(CAC):

Factor in lead generation, marketing, hardware subsidies, sales commissions, and onboarding expenses. Keep CAC low without compromising service quality.

11. Average Monthly Processing Volume per Merchant:

Estimate transaction volume realistically, considering vertical mix such as retail versus online. Remember that high-volume merchants help you recover acquisition costs more quickly, improving your cash flow and overall profitability while balancing your portfolio between small, medium, and enterprise-level accounts for steady growth.

12. Churn Rate (Monthly %):

Track monthly churn rigorously, segmenting by vertical, cohort, and sales channel. Target under 3% by accelerating activations, offering 24/7 first-line support, and keeping pricing and statements transparent.

Use health scores, timely dunning alerts, and targeted win-back offers to stabilize MRR, protect lifetime value and reduce preventable churn.

13. Chargeback & Fraud Reserve:

Hold a reserve equal to 1-2% of total processing volume to be held as reserve capital to cover chargebacks, fraud losses, and disputes. Keep funds segregated, review levels quarterly by vertical risk, and increase during peak seasons.

14. Gross Margin & Payback Period:

Calculate your gross margin by subtracting interchange and partner fees from total revenue to measure true profitability. Track payback on customer acquisition and hardware costs, aiming for recovery within 12 months.

Use dashboards or accounting tools to monitor real-time performance. Monitor each merchant’s lifetime value(LTV), monthly residual income, and profitability. This will help you predict scaling needs such as whether hiring new agents, increasing inventory, or expanding into new territories.

Also Read: Smart POS Systems

Step-4. Product Packaging: What you will sell:

A strong product offering is the foundation of your payment franchise. With Ace Merchant Processing, you can build a well-rounded suite of solutions which is designed for retail, e-commerce, and service-based merchants.

1. Card-present POS and countertop terminals:

Card-present POS and countertop terminals are EMV and NFC-enabled devices that support chip, tap, and mobile wallet payments. They ensure fast, secure, and compliant in-person transactions, reducing fraud while improving customer convenience.

2. Mobile payments (mPOS):

Mobile payments(mPOS) use compact, Bluetooth-enabled card readers that connect to smartphones or tablets, allowing secure payments anywhere.

mPOS systems enable instant transactions, digital receipts, and real-time reporting making payment acceptance flexible, fast, and reliable in any business environment.

3. Payment gateway for e-commerce:

Payment gateway integrates smoothly and effortlessly with top e-commerce platforms such as WooCommerce, Shopify, and Magento, enabling businesses to accept online payments effortlessly.

They ensure secure checkout experiences with PCI-compliant encryption, support multiple payment methods, and offer features such as fraud prevention, instant settlements, and real-time transaction tracking for smooth and reliable order processing.

4. Hosted payment pages and invoicing:

Hosted payment pages and invoicing solutions simplify online payments for service-based and subscription businesses. It enables recurring billing, securely stores customer cards, and allows clients to pay invoices instantly via a secure hosted link.

With automated reminders and real-time payment tracking, businesses get to improve cash flow and deliver a smooth billing experience.

5. Virtual terminal:

A virtual terminal allows merchants to key in card details in order to accept payments without a physical reader which is ideal for phone orders, remote billing, and call centers.

It supports one-time and recurring charges, tokenized saved cards, AVS or CVV checks, refunds, and voids, with PCI-compliant security, user permissions, transaction reporting, and receipts and audit logs.

6. Security add-ons:

Security add-ons which include tokenization that replaces card numbers with non-sensitive tokens, PCI-DSS guidance with gap assessments and SAQ templates, and strong chargeback management.

Also integrate 3-D Secure, AVS or CVV checks, velocity rules, device fingerprinting, and encryption to reduce fraud. Centralized dashboards track customer disputes, automate evidence, and maintain audit trails, alerts and reporting.

Such core products help to make your franchise a one-stop payment solution provider.

7. Value-Added Features That Differentiate Your Payment Offering:

In today’s competitive payment ecosystem, it is not enough to simply process transactions. Merchants expect speed, insight, and flexibility from their providers.

It is only by offering effective features on top of your core gateway that you can build deeper loyalty, justify premium pricing, and create upgrades which is essential for every stage of business growth.

8. Next-Day Settlements:

Every small business centers around cash flow. Offering next-day settlements offers merchants quicker access to their funds mostly within 24 hours that helps them to manage payroll, restock inventory, and cover operational costs without any delays.

When supported by Ace’s intelligent routing and risk engine, these fast payouts remain secure and compliant. Offer instant or same-day settlements to qualified high-volume merchants, creating a clear advantage in markets where competitors still take 2-3 days to release funds.

9. Local Language Receipts and Support:

Localization helps you to build trust. Offering receipts, invoices, and support in the language that the merchants prefer ensures comfort for regional businesses or cross-border markets.

So whether it is Hindi, Spanish, or Arabic, multilingual capabilities show respect for local culture and also make compliance conversations easier to understand.

10. Integrated Loyalty and Gift Card Systems:

Modern consumers value recognition and rewards. So by offering built-in loyalty and gift card systems, your payment platform becomes more than just a transactional tool and becomes a growth engine.

Merchants get to issue branded gift cards, reward repeat purchases, and track redemption data directly from their dashboard which not just helps to improve higher order value but also motivates repeat customers and word-of-mouth referrals.

11. Financing Options:

One of the biggest challenges for small and mid-sized merchants is that they have access to capital. By partnering with lenders or fintech providers allows them to offer working capital advances or equipment leasing through your merchant portal.

Link repayments to sales volume so payments rise and fall with revenue, keeping cash flow manageable while the business grows. It will place your payment solution as a trusted business partner rather than a simple processor.

12. Analytics Dashboard:

Data is power. When merchants have access to a real-time dashboard they get to view daily sales, top-selling products, analyze customer behavior, and export reconciliation data for accounting.

Visual insights and automated reports help to transform payment data into actionable intelligence through which merchants can do smarter marketing, and staffing decisions.

13. Tiered Offerings for Growth:

To make adoption simple, bundle such value-added features into clear, scalable plans which are Starter, Growth, and Enterprise. Every plan can gradually show features like quicker settlements, deeper analytics, and access to financing.

Also Read: Top Retail Payment Trends Every Business Should Know

Step 4 — Technical Integration & Operations

Smooth and effortless technical setup and efficient operations form the backbone of a strong payment ecosystem. By combining clear documentation, smooth onboarding, organized logistics, and transparent reporting through which you can deliver a consistent and scalable merchant experience.

1. Access to Ace’s Technical Stack:

Ensure partners have full access to Ace’s technical resources. Offer detailed API documentation which includes tokenization, transaction capture, refunds, webhooks, and settlements.

2. Quick, Low-Friction Onboarding Flow:

Design a secure, digital onboarding process which collects merchant data such as business name, tax ID, owner ID, bank details via encrypted forms. Submit the information to Ace’s underwriting API for real-time approval.

Once approved, automatically generate credentials, configure terminals or gateways, and send welcome assets. Integrate automated reconciliations via email or SMS and link exception cases to Zendesk for resolution.

3. Terminal Provisioning & Logistics

Maintain a small terminal stock for quick shipping or use Ace’s drop-ship service. Create SOPs for shipping, activation, and on-site setup and run a return-refurbishment-redeploy cycle to reduce waste and maximize hardware utilization.

4. Reconciliation & Reporting

Provide daily and monthly settlement summaries with downloadable CSV exports. Integrate reconciliation data via SFTP or API for automated accounting. Offer a branded merchant portal where users can view transactions, settlements, and performance analytics in real time.

Also Read: Retail Payment Platforms for Shaping the Future of Retail

Step 5 — Underwriting, KYC & Risk Management

For building a stable, compliant, and profitable payment franchise, it is essential to do effective underwriting and risk management. With proper verification, chargeback control, and fraud prevention protect both merchants and your reputation.

1. Tiered Underwriting:

Every merchant has a different risk profile. Use a tiered approach where Low risk merchants go through simple ID and bank validation for instant approval. Medium Risk merchants provide business documents like lease or inventory proof while high risk merchants require manual review, high reserves, and daily transaction limits. This framework delivers fast approvals without compromising security.

2. KYC & AML Automation:

Integrate Ace’s API or third-party tools for automatic ID scanning, address verification, and instant bank validation. By automating KYC helps to reduce manual errors, faster onboarding and keeps your franchise compliant with AML regulations.Store only necessary data securely.

3. Chargeback & Dispute Playbook:

Develop a 7-day SLA for chargeback responses. Maintain a standardized evidence pack like receipts, IP logs, or customer signatures and educate merchants to use clear billing descriptors and pre-authorizations to avoid unnecessary disputes.

4. Fraud Prevention Tools:

Use AVS or CVV checks, 3D Secure, velocity, and geolocation monitoring, and ML-based fraud scoring to detect anomalies before they cause business losses.

5. Continuous Monitoring:

Ensure you regularly review merchant activity and chargeback ratios. Automated alerts and periodic audits help you identify unusual trends early, ensuring financial safety and operational trust.

Also Read: Contractor Payment Solutions

Step 6 — Merchant Onboarding & Support Playbooks

A smooth and effortless onboarding process and responsive support system build merchant confidence and reduce early churn. Standardizing activation, training, and escalation ensures consistent service across your payment franchise.

1. 0→30 Day Activation Checklist:

Design a step-by-step activation plan to guide merchants through their first month.

Day 0: Send a branded welcome email with documentation and activation instructions to clients.

Day 1-3: Ship and activate terminals, generate gateway credentials, and test transactions.

Day 4-10: Verify first payments, confirm reconciliation accuracy, and test receipts.

Day 11-30: Conduct a review call to resolve issues, configure POS features, and introduce cross-sell opportunities.

Automate all steps through your CRM to assign tasks, track progress, and trigger reminders.

2. Support Tiers & SLAs:

Set a clear support level. Tier 1 handles basic merchant queries, refunds, and terminal troubleshooting. Tier 2(Ace) addresses underwriting or settlement issues. For ensuring timely resolutions define escalation contacts and strict SLAs.

3. Training & Documentation:

Provide quick-start guides, short videos, and FAQ flowcharts so merchants can self-solve common issues, reducing support volume, faster onboarding, and improving overall satisfaction.

Also Read: Hospitality Merchant Services for Hotels and Resorts

Step 7 — Sales & Go-to-Market:

Your sales and go-to-market strategy determines how effectively your payment franchise acquires and retains merchants. So by focusing clearly on the right verticals, channels, and messaging ensures faster traction and higher conversion rates.

1. Target Verticals & Ideal Customer Profile (ICP):

Begin with 2-3 high frequency transaction sectors like restaurants, retails, salons, and SMB eCommerce. These businesses rely on fast, reliable payments and value hands on-support.

Build vertical-specific playbooks with customized scripts, ROI calculators, and case studies to address their unique needs.

2. Sales Channels:

Adopt a multi-channel model such as field sales for in-person retail, inside sales for service and eCommerce merchants and partnerships with POS vendors, accountants, and agencies. Use digital marketing like local SEO, Google Ads, and landing pages to capture inbound leads.

3. Sales Collateral:

Equip your team with pricing one-pagers showing transparent cost comparisons, terminal demo videos, and real merchant success stories. Visual trust badges help to reinforce credibility.

Also Read: Smart Payment Solution for Gaming and Esports

Step 8 — Marketing, Lead Generation & Retention

A strong marketing engine fuels consistent merchant growth. Combine local visibility, digital outreach, and relationship-based retention to build a sustainable payment franchise which merchants trust and recommend.

1. Local & Digital Acquisition:

Begin by optimizing your Google Business Profile and Map listing to capture high-intent local leads. Run PPC campaigns with vertical-specific landing pages. Use content marketing to build credibility through blogs. Add case studies highlighting local success stories.

2. Promotions & Incentives:

Run limited-time offers like free terminal setup with a 12-month contract or 90 days with no interchange markup. Build a referral program rewarding merchants with credits or bonuses for each new signup they refer which strengthens word-of-mouth marketing.

3. Retention & NPS:

Be proactive and run monthly onboarding check-ins, quarterly business reviews for performance insights, and automated NPS surveys to measure customer satisfaction. Re-engage inactive or at-risk merchants with win-back campaigns, personalized offers.

Step 9 — Metrics, Performance & Scale

1. Core KPIs:

Track key growth and profitability metrics such as MRR, GMV, churn rate, chargeback ratio. These indications show franchise health, merchant satisfaction, and revenue efficiency.

2. Operational Dashboards:

Use real-time dashboards to monitor merchant onboarding status, terminal activations, support tickets, and settlement accuracy. Automating reports through BI tools helps to visualize trends and identify challenges.

Step 10 — Scaling: Teams, Tech & Partnerships

1. Organizational Growth:

As your payment franchise expands, make sure you grow your team strategically. Start with 1-3 sales representatives or SDRs to improve acquisitions, onboarding specialists to manage merchant activations and remote support agents for 24/7 coverage.

2. Technology Investments:

Ensure you invest early in tools like CRM or merchant portal, a ticketing system, and data integration tools. Use business intelligence dashboards to foresee sales, churn rates, and improve decision making.

3. Strategic Partnerships & Risk Controls:

Collaborate with POS vendors, banks, and industry associations for bundled solutions and co-marketing. Avoid risks like unclear pricing, slow onboarding, weak fraud management, or poor escalation channels.

Conclusion:

Establishing a payment franchise with Ace Merchant Processing is one of the most rewarding ways to enter the fintech and merchant services sector. And with a solid foundation, transparent pricing, and scalable systems, you can develop a sustainable business which delivers real value to merchants while generating consistent recurrent revenue.

By following each step from defining your model, setting up legal and commercial structures, packaging services, to building strong underwriting, onboarding, and support processes, you lay the groundwork for long-term success. Combining reliable technology, strong compliance, and customer-centric operations that ensures your franchise stands out in a competitive market.

As your merchant base grows, use data-driven dashboards, automation tools, and strategic partnerships to grow efficiently. Focus on trust, local presence, and quick problem resolutions which is essential for any successful payments brand.

While you partner with Ace Merchant processing, you not just gain best-in-class infrastructure, but also the expertise, tools, and reputation to grow confidently. Your franchise becomes more than just a reseller, it becomes a trusted local payments partner for every business you serve.