For modern contractors, plumbers, electricians, HVAC technicians, landscapers, and other on-site professionals, it is essential to have fast and secure payment collection to maintain healthy cash flow.

The era of waiting for checks to clear or mailing paper invoices that take weeks to process. Contractor payment solutions like tap-to-pay and mobile payment options which have transformed how service professionals get paid.

If you are accepting deposits before a remodel, collecting payment after a repair, or closing a landscaping project, then having the ability to be able to use contactless payments on the job site helps you get paid faster, build trust, and reduce paperwork.

Mobile payment systems for contractors allow you to accept cards, digital wallets, and NFC tap payments directly from your smartphone or tablet without large terminals or point-of-sale setups required.

With features such as instant receipts, automatic reconciliation, and real-time payment tracking allows you to handle transactions smoothly even in the field. Additionally, softPOS and tap-to-phone technology allows you to accept Apple Pay, Google Pay, or contactless card payments directly from your device.

By adopting mobile payment solutions which combine tokenization, encryption, and PCI compliance, contractors can reduce fraud risk giving a professional and technically forward image.

These tools also integrate with job management, invoicing, and accounting systems, that makes bookkeeping simpler. Through this guide we will explore the best contractor payment technologies, from tap-to-pay readers to mobile invoicing apps, and outline how these innovations streamline payments, improve efficiency, and help contractors to focus less on chasing money rather than focus more on growing their business.

Also Read: The Future of Retail Payments

How Tap to Pay Works (Cards, Phones, and Wallets)

Tap to pay is a contactless way to accept payments using short-range radio technology. A contactless card contains a small antenna around the EMV chip that activates when held 1–3 inches from a compatible terminal, allowing the two devices to communicate securely using RFID technology.

In milliseconds, the terminal and the card perform a cryptographic handshake that creates a unique, one-time code for that purchase so even if someone could somehow see the data, it wouldn’t be reusable. Because the signal only travels a few inches and each transaction is uniquely tokenized, tap payments are both fast and secure.

Also Read: What is Payment Processing Software

Tap to Pay with Phones(NFC+Mobile Wallets):

Modern smartphones and many wearables use NFC(near-field communication) which is similar to RFID, to function like a contactless payment card.While you hold the device near a payment terminal, a secure element activates and sends a token with a unique cryptogram instead of the actual card number, keeping each transaction secure.

Such design reduces fraud and keeps primary account numbers out of merchant systems.The mobile wallet app manages the process of adding a bank-verified card once, unlocking with your fingerprint or passcode, tapping your device, and the terminal sends the authorization request within a second. Wallets can also pass device authentication and other risk signals that often improve approval rates.

Some such popular options are Apple Pay, Google Pay, and more. These mobile wallets let customers make contactless credit or debit payments using just their devices without any physical card required, delivering faster checkout, more convenience, and more security for both consumers and merchants in everyday transactions.

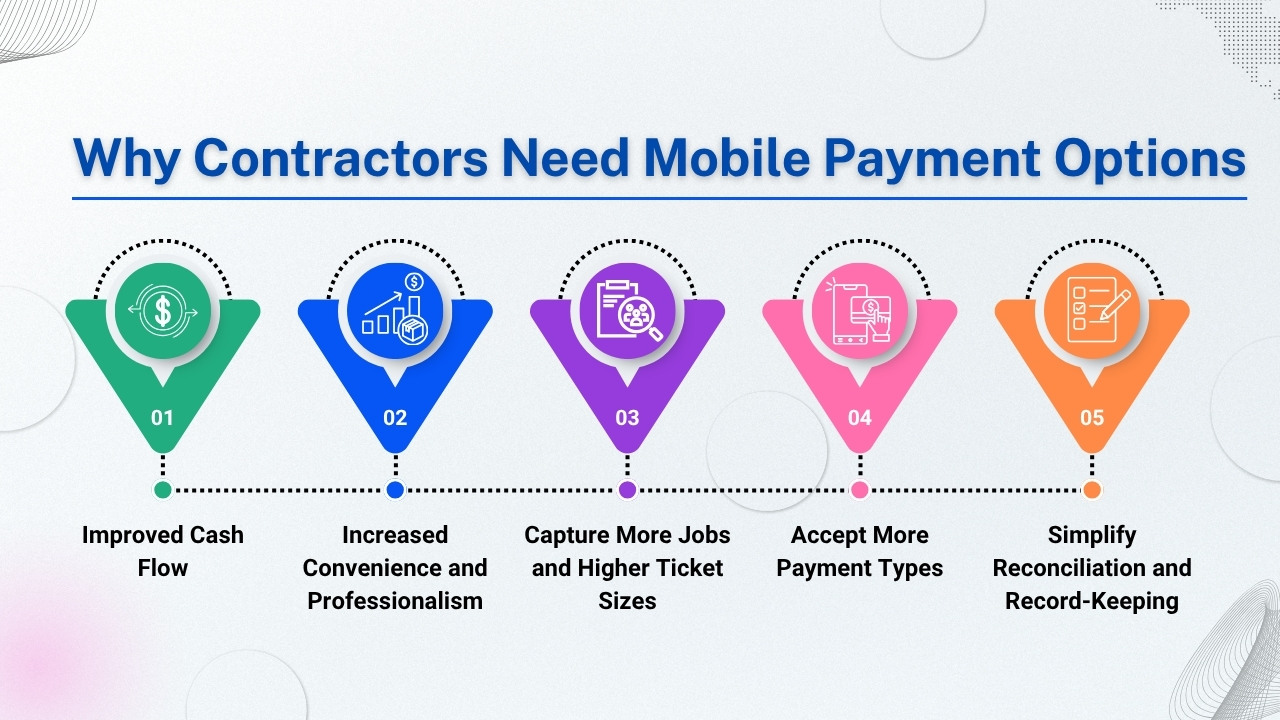

Why Contractors Need Mobile Payment Options

1. Improved Cash Flow:

After finishing a job and handing over an invoice, waiting days or weeks for payment can strain your cash flow and working capital.Accepting payments on the spot via credit/debit card, mobile wallet, or tap-to-pay means you can collect payment when the job is fresh in the customer’s mind, then focus on the next task. Such solutions help to remove the lag between job completion and cash inflow.

2. Increased Convenience and Professionalism:

Today customers expect convenience as they are mostly habitual to paying with credit cards, Apple Pay, Google Pay, contactless cards, or digital wallets even on-site. Making payment simple and offering instant receipts helps build trust, and boost customer satisfaction. Recent research suggests that mobile card payment solutions such as Ace Merchant Payment Solution can increase sales by almost 30%.

3. Capture More Jobs and Higher Ticket Sizes:

When you accept payment on-site, you remove friction while the customer pays immediately and you avoid the need for follow-ups.Card payments usually cause higher spending than cash or checks, and offering them on-site can encourage customers to select add-ons or upgrades.

Also Read: Retail Payment Platform Shaping the Future of Retail

4. Accept More Payment Types:

Older payment methods like cash, cheque restrict you. While mobile payments allow you to accept chip and PIN, contactless, tap to phone, wallet payments, even QR codes. By providing flexible payment options helps avoid lost jobs by ensuring clients can pay quickly and conveniently.

5. Simplify Reconciliation and Record-Keeping:

Modern mobile payment platforms include invoicing, automatic receipts via SMS or email, integrated reporting, and transaction dashboards. It reduces administrative burden like fewer handwritten receipts, fewer lost invoices, fewer reconciliations.

Top Mobile Payment Solutions for Contractors

Contractors now have multiple ways to collect payments directly in the field. So even if you prefer simple mobile card readers, fully featured invoicing apps, or digital payment tools, the right setup depends on your business size, connectivity, and workflow.

Below are the three main categories of mobile payment solutions every contractor should consider.

1. Plug-and-Play Mobile Card Readers:

Mobile credit card readers are small devices that connect to your phone or tablet via Bluebooth. It allows you to swipe, dip, or tap a customer’s card instantly. Many include offline modes for remote job sites and quick setup through a simple companion app.

Fees usually range from 2.6%-3% per transaction, and most require no monthly subscription. For contractors who value speed, simplicity, and immediate payment confirmation such devices are a dependable option.

2. All-in-One Invoicing and Payment Apps:

Most payment options combine invoicing, payment processing, and accounting in one place. You can create estimates, send invoices, and accept card or ACH payments right from your phone.

Such platforms automatically record transactions, making bookkeeping simpler. ACH transfers are ideal for large invoices because of lower fees, while credit cards offer instant payment and convenience.

Also Read: Restaurant Credit Card Processing

3. Peer-to-Peer and Bank Apps:

For small or one-off jobs, peer-to-peer and bank apps offer quick, fee-free transfers. While they are convenient, they lack features like automatic receipts, chargeback protection, and accounting integration. Contractors should use them cautiously for repeat clients or small jobs and depend on professional payment systems for larger, invoiced-backed projects.

Together such mobile tools help contractors improve cash flow, reduce paperwork, and deliver faster, convenient, and more security.

4. mPOS Devices:

Mobile point-of-sale(mPOS) devices are small card readers(chip+contactless) that pair with a smartphone or tablet. When you plug or connect the reader via Bluetooth or USB and the mobile app handles the transaction.

Such devices are ideal for in-job environments, service vans, remote sites. Due to the affordability and portability make mPOS devices well suited for one-person or small teams.

5. SoftPOS / Tap to Pay on Phone:

SoftPOS refers to converting a smartphone or tablet itself into a payment terminal in which no external reader is needed. It is an attractive option for mobile contractors because you may already have the smartphone; just install the right app and you are ready.

6. Invoicing + Payment Link + QR Code:

Another approach where you send an invoice through the payment platform or app, the client sees it on their phone or email, taps a link or scans a QR code, and pays instantly. It is useful when the service is completed and you are off-site or the customer is remote.

7. Integrated Contractor Payment Suites:

Some platforms combine everything into a single smooth workflow for contractors which includes estimate and job approval to service completion, mobile payment, and instant invoicing. They integrate job management, payment, reporting, and keep everything in one place.

Also Read: Retail Payment Platform Shaping the Future of Retail

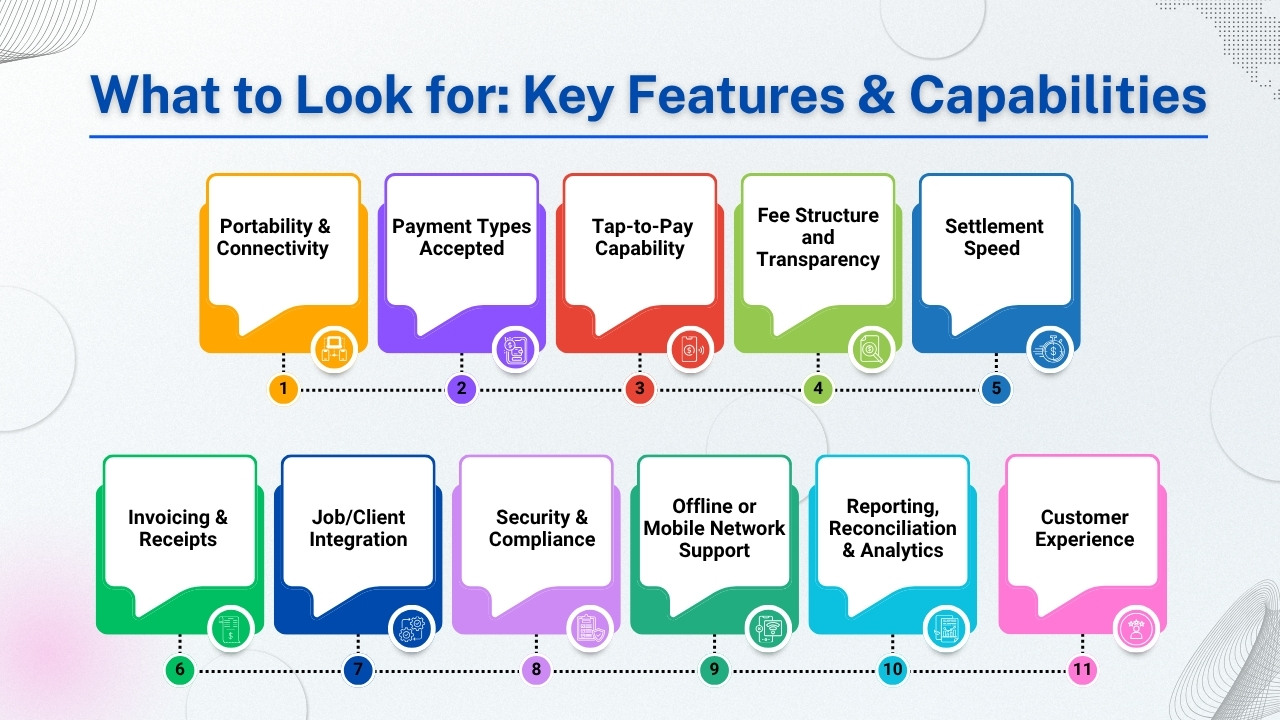

What to Look for: Key Features & Capabilities

When choosing the right payment solution for your contracting business, it’s essential to evaluate not just cost, but also usability, reliability, and integration with your daily operations. Below are some of the most important features and capabilities to look for before selecting any mobile or tap-to-pay payment system.

1. Portability & Connectivity:

Make sure your payment solution functions smoothly wherever you work, whether at a client’s home, on a job site, or from your service vehicle. Devices should operate smoothly on Wi-Fi or cellular data and ideally include an offline mode to process payments in weak-signal areas.

2. Payment Types Accepted:

Select a system that supports multiple payment options like chip and PIN, contactless cards, mobile wallets like Apple Pay, Google Pay, and Samsung Pay, as well as QR codes or NFC tap-to-phone. The more flexible options you provide, the easier it is for customers to pay.

Also Read: Top Retail Payment Trends

3. Tap-to-Pay Capability:

If you prefer not to carry extra hardware, look for softPOS(tap-to-phone)options that allow your smartphone or tablet to accept contactless payments directly.

4. Fee Structure and Transparency:

Understand all associated costs upfront which include transaction fees, flat charges, monthly fees, equipment costs, and contract terms. Transparent pricing helps you predict expenses accurately.

5. Settlement Speed:

Quick access to fund matters so opt for providers offering next-day funding or same-day deposits to maintain strong cash flow.

6. Invoicing & Receipts:

The best systems allow you to send invoices and digital receipts instantly via email or SMS, track payments, and keep transaction history in one place.

7. Job/Client Integration:

Integration with your existing CRM, scheduling, and estimating software ensures all payments are linked to jobs, clients, and invoices automatically.

8. Security & Compliance:

Your system should support EMV, tokenization, and end-to-end encryption(E2EE) while meeting PCI DSS compliance standards to protect cardholder data.

9. Offline or Mobile Network Support:

In remote areas, having queued transaction support and automatic syncing when reconnected helps ensure you never lose a sale.

10 .Reporting, Reconciliation & Analytics:

Detailed reporting helps track payments by job or client, monitor trends, export financial data, and simplify bookkeeping or tax preparation.

11. Customer Experience:

A smooth, professional tap-and-pay experience with easy signature and tip options builds trust, encourages repeat customers, and strengthens your brand image.

While a contractor payment solution that balances these features delivers not just speed and convenience but also professionalism, security, and long-term business efficiency.

Also Read: How to Choose the Right POS System for Your Business

Cost & Pricing Considerations for Contractors

When selecting a mobile payment solution, it is essential to understand the pricing model and cost structure. The right payment plan can protect your margins, improve cash flow, while the wrong payment plan can quietly erode your profits over time. Below are some essential pricing factors to consider before you commit to a provider.

1. Fee Models:

Payment processors use one of two models either flat-rate or interchange-plus. A flat-rate plan charges a fixed percentage on every transaction regardless of card type or volume. It’s simple and predictable which makes it a great option for small or seasonal contractors with low monthly sales.

However as your business grows, interchange-plus pricing which passes through the actual card network fee and a small markup that becomes more cost-effective and transparent. It scales better for high-volume operations where every fraction of a percent adds up.

2. Device Costs & Subscriptions:

Some payment providers require you to purchase or lease hardware like mobile reader or terminal while others offer no-hardware solutions through softPOS or tap-to-phone technology.

Evaluate upfront costs, monthly fees, and potential long-term commitments. Check for minimum usage requirements, inactivity fees, or hidden surcharges that might surprise you. For many small contractors , a simple pay-as-you-go plan with low setup costs offers the best flexibility.

3. Settlement Timing:

Speed of funding is important in the contracting world. Select a provider that offers next-day or same-day deposits, especially if you depend on quick cash flow to pay suppliers, subcontractors, or material vendors. Understand how the processor handles weekends, holidays, and batch cutoffs. Some delay settlements until the next business day, which could impact your operations.

Also Read: Smart POS Systems the Secret to Faster Checkouts

4. Risk & Chargebacks

On-site transactions have unique risks like job delays or client disputes. The best solutions include fraud detection, chargeback assistance, and clear refund policies to help protect your business. So look for tools that provide detailed transaction logs and digital receipts to strengthen your case during any dispute.

5. Tax & Service Job Management:

If you bill for multiple components like labor, materials, travel fees, or taxes ensure your payment platform supports itemized billing. This simplifies accounting, reporting, and tax filing while ensuring transparency with customers.

6. Geographic & Network Constraints:

If your business operates across regions or countries, verify that your provider supports local card networks and currencies. Some softPOS or tap-to-pay solutions have device or region limitations, so always confirm compatibility before rollout.

Also Read: Hospitality Merchant Services for Hotels and Resorts

Security & Compliance Essentials

Accepting digital and contactless payments gives contractors flexibility but it also comes with responsibility. Protecting sensitive customer data is crucial to maintain trust, meet regulatory requirements, and avoid costly security breaches. Below are some key security and compliance areas every contractor should understand and implement.

1. EMV & Tokenization:

Always use EMV-certified readers or softPOS solutions which support tokenization. EMV chip transactions use dynamic data to avoid cloning while tokenization replaces the raw card number(PAN) with a secure, non-sensitive token. It ensures your system never stores or transmits actual card data, reducing your risk.

2. Encryption / P2PE:

Your payment solution should feature end-to-end encryption(E2EE) or point-to-point encryption(P2PE) from the device to the processor. It means that even if data were intercepted then it would be unreadable. End-to-end encryption is a must feature for card-present and mobile payments.

3. PCI Compliance:

Contractors using mobile payment apps still come under PCI DSS. Check with your provider about what Self Assessment Questionnaire type applies and what should be completed annually. Maintaining PCI compliance helps avoid penalties and ensures secure data handling.

4. Secure Devices:

Consider any smartphone or tablet used for payments as a payment terminal. While it is essential to keep the operating system up to date, use strong PINs or biometric locks and restrict app installations to avoid malware. So avoid sharing devices between staff without proper permissions.

5. Data Logging & Reconciliation:

It is essential to maintain correct records of every transaction like timestamps, receipts, and job references. This data supports auditing, tax reporting, and dispute resolution.

6. Offline / Queued Transactions:

If you use offline mode, define transaction limits and reconcile queued payments immediately after reconnecting to avoid errors or duplicates. It reduces the risk of duplicate charges or unprocessed transactions.

7. Chargeback Management:

Select a provider offering chargeback support and clear workflows for submitting evidence like signed receipts, timestamps, and job notes. Tap-to-pay systems usually create cleaner digital records, making dispute resolution easy and reducing administrative burden.

By applying best practices, contractors can confidently accept mobile payments by keeping security strong and compliance effortless.

Integration with Contractor Workflow

Implementing a mobile payment solution is not about just plugging in a card reader rather creating a smoother, faster, and more organized process from the first estimate to the final receipt.

While the aim is to make payments a smooth part of your everyday operations. Below are some key stages that show how mobile payment systems integrate perfectly into a contractor’s workflow.

1. Estimate & Job Scheduling:

Your payment process begins before the job starts. While you send an estimate, let clients approve it digitally and schedule the work immediately. You get to include deposit or best payment options in the estimate which helps secure commitment and improve cash flow. Implementing these steps ensures both parties know what to expect financially before work begins.

2. Invoicing & Payment Request:

Once the job is completed create an invoice using your mobile app. Many platforms let you send a payment request through email or SMS, allowing clients to pay instantly using credit cards, debit cards, or ACH transfers. It reduces paper work, invoicing delays, and gets faster funds.

3. On-Site Payment Capture

For jobs completed on-site, mobile readers or tap-to-pay devices allow you accept payment instantly via card, wallet, or QR code. While the system automatically records transactions and sends email or text a digital receipt to the customer within seconds.

Also Read: Restaurant Payment Platforms Shaping the Future of Retails

4. Job Completion & Documentation:

Mark the job as completed in your system once you receive payment. Though your CRM or field-service app can automatically update job status, store payment data, and sync with accounting software. It removes double entry and keeps your books and records in real time.

5. Reporting & Reconciliation:

At the end of each day or week, review payment summaries on the basis of job, customer, and service type. Export data directly into your accounting platforms in order to match deposits and also reconcile transactions. Automated reports simplify tax preparation and highlight trends like top-paying clients or most profitable services.

6. Customer Follow-Up & Upsells:

Ultimately use payment and job data to empower marketing and customer retention. Also schedule reminders for future maintenance, offer loyalty discounts, or suggest upgrades based on previous work. Because of integrated payment tools and CRM data, you get to personalize offers and build long-term customer relationships which drive repeat business and higher revenue.

Implementation Steps – Step by Step

Successfully deploying a mobile payment solution for your contract business requires not just signing up for an app but it requires thoughtful setup, testing, and continuous optimization to ensure it fits smoothly into your daily operations. By following these step-by-step implementation guidelines to get your system running smoothly from the first day.

1. Evaluate Payment Providers:

Start by identifying payment providers which specifically serve contractors and field-service businesses. Look for important features like mPOS or softPOS, mobile wallet support(ApplePay, GooglePay, integrated invoicing, and job management capabilities. Check whether the platform perfectly matches your current workflow and tools like CRM or scheduling software.

2. Review Fee Structure & Settlement Terms:

It is essential to understand the pricing and funding policies of the provider. So compare flat-rate versus interchange-plus fee structures and calculate your estimated costs on the basis of transaction volume. Inquire about settlement timing like how many weekends, holidays, and about batch cutoffs that affects payouts so your cash flow remains predictable.

3. Check Hardware & Device Requirements:

Verify compatibility between your devices and the provider’s system. Ensure the payment app works with your smartphone or tablet, and test any required card readers or tap-to-pay features. If you often work in remote areas, confirm the system supports offline mode or queued transactions.

4. Review Security & Compliance:

Confirm that the provider provides strong security like PCI compliance, tokenization, and E2EE. Understand your role in maintaining compliance, including service locking, password management, and data storage policies. Also verify support for dispute and chargeback management to protect against fraud.

5. Pilot the Solution:

Test the system on a few small jobs before a full rollout. Capture payments on-site, send digital receipts, and verify settlement accuracy. Track the process from payment initiation to bank deposit to ensure everything works as expected.

6. Train Your Field Team:

Once testing is successful, train your staff thoroughly. Demonstrate how to accept payments, generate invoices, send receipts, add tips or adjustments, and handle refunds. Provide troubleshooting steps and security best practices.

7. Go Live Across All Jobs:

Launch the system company-wide. Encourage customers to use the new payment method and monitor adoption. Consistent usage will streamline reconciliation and improve cash flow visibility.

8. Monitor Reporting & Optimize:

Track daily and weekly metrics like payment volume, declines, and settlement timing. Identify jobs still invoiced manually and shift them to real-time collection. Evaluate how the system reduces late payments and improves efficiency.

9. Expand Value:

Once your base process is stable, extend the system to include digital quotes, retainer plans, and recurring payments. This turns your payment solution into a full business platform which saves time, strengthens client relationships, and maximizes revenue.

Conclusion

For today’s contractors, mobile and tap-to-pay payment solutions are more than just modern conveniences which are business essentials. So even if you are a plumber collecting payment at a customer’s home, or an electrician finishing a repair, being able to accept payments instantly and securely transforms the way you do business. It removes delays, reduces paperwork, and gives customers the convenience which they expect in a digital-first world.

The right contractor payment solution integrates directly into your workflow that includes estimate, scheduling, invoicing, payment, and reconciliation so every transaction is monitored, transparent, and compliant.

Features like tokenization, end-to-end encryption, and PCI compliance protect sensitive data, while tools like mobile invoicing. ACH transfers, and tap-to-pay speed up collections and simplify accounting.

With instant receipts and integrated reporting you save time on admin tasks and focus more on what matters like delivering great service and winning more jobs.

As the industry continues to move toward contactless and mobile payment technology, adopting these tools early helps contractors stay ahead of competitors and meet rising customer expectations.

Whether you use a simple mobile reader, an all-in-one payment app, or a full-service softPOS system the aim is the same to make payments smooth, secure, and fast.

By adopting mobile and tap-to-pay systems, contractors can enjoy better cash flow, fewer disputes, and happier clients turning every completed job into an opportunity for stronger customer relationships and stable business growth. The future of contracting is contactless, connected, and built around getting paid on time, every time.