Securing a high-risk merchant account is one of the biggest challenges faced by businesses who are operating in regulated, high-liability, or chargeback prone industries.

Whether you sell CBD, Kratom, supplements, adult products, travel services, coaching programs, dropshipping goods, or financial services, you have likely discovered that most traditional payment processors reject such applications instantly.

This reality sends thousands of merchants searching for terms like “high-risk merchant account instant approval,” hoping to discover a quick, hassle-free way to start accepting payments online.

But the truth is more complex as instant approval does not exist for legitimate high-risk processing. Because of federal KYC or AML laws, card-network regulations, underwriting requirements, and industry-specific compliance rules make it impossible for banks to approve a high-risk merchant without reviewing their documents, verifying business legitimacy, and evaluating exposure to chargebacks, fraud, refunds, and regulatory risk.

What is realistic, however, is fast approval sometimes in as less as 24 hours when a merchant submits complete documentation and clearly meets the processor’s review criteria.

Modern high-risk payment providers now use streamlined onboarding and underwriting, so they can rapidly assess your business model, website compliance, CBD COAs, supplier transparency, shipping practices, and refund policies.

When handled correctly, it can lead to a near-instant pre-approval and rapid deployment of a merchant account.

In today’s digital marketplace, understanding how high-risk payment processing works is essential. Domestic acquiring banks, offshore processors, and high-risk gateways all use different criteria to determine whether a merchant qualifies.

Factors like business model, legal status, regulatory sensitivity, transaction patterns, and operational stability all influence approval speed and pricing.

Through this detailed blog will break down everything you need to know about high-risk merchant account instant approval, including how real underwriting works, how to speed up approval, which industries qualify, what documents you need, how reserves and rolling payout function, and how to avoid scam processors promising “no-documents” onboarding.

Also Read: Top 5 Features Every Retailer Should Look for in a Modern Payment Terminal

What is a High-Risk Merchant Account?

A high-risk merchant account is a type of payment processing account which is designed for businesses that function in industries with higher chances of fraud, chargebacks, or regulatory scrutiny.

Rather than blocking these businesses entirely, Payment Service Providers(PSPs) offer high-risk accounts so that they can still accept credit and debit card payments but under tighter rules and at higher costs than low-risk merchant accounts.

Processors assess every new merchant on the basis of risk exposure. If your business model, product, target market, or past processing history suggest a higher chance of disputes, refunds, or compliance issues, you will be classified as a high-risk merchant.

On the contrary, low-risk merchant accounts have predictable transactions, low chargeback ratios, and minimal regulatory oversight. While it’s also possible to move from low-risk to high-risk.

For instance, if your chargebacks increase, you start selling regulated products such as CBD or supplements, or your refund patterns change, your provider may reclassify your account as high-risk.

High-risk merchants typically face:

- Fewer processing options

- Higher processing fees

- Possible rolling reserves

- Stricter contract terms and monitoring

Even though it’s not ideal, a high-risk merchant account is often the only fully compliant way for some businesses to keep processing card payments and stay operational online or in-store.

Also Read: Top Retail Payment Trends Every Business Should Know

High-Risk Merchant Account: What Verticals Are Considered High Risk?

Understanding whether your business falls into a high-risk category, even if these labels are sometimes broad or don’t fully reflect how you actually operate. Just because an industry has historically experienced higher chargebacks but it does not mean your specific business will face excessive disputes.

However, payment processors depend on industry-wide data when assessing risk, so knowing where your business comes under helps you prepare for underwriting and approval requirements.

Common high-risk industries include:

Auctions, bail bonds, card-not-present firearms, CBD and Delta products, coaching or online education, adult products, collection agencies, subscription or continuity offers, credit repair, online dating, debt consolidation, digital goods, document prep, e-cigarettes, e-commerce, firearms, furniture and electronics, gambling, nutraceuticals, marijuana-related services, money transmitters, MLM programs, outbound marketing, pawn shops, quasi-cash services, recurring billing programs, timeshare exit services, tobacco and nicotine products, travel services, and vape products.

Also Read: How to Build Payment Franchise With Ace Merchant Processing

How Are Businesses Classified as High-Risk?

Payment processors classify businesses as high-risk based on how much financial exposure, chargeback potential, and regulatory complexity they present.

This evaluation determines not only whether a merchant qualifies for a standard merchant account but also what underwriting requirements, processing fees, and contractual terms will apply.

One of the strongest indicators of high-risk status is transaction behavior including monthly processing volume of $20000 or more, where average ticket sizes are above $500, or historically increased chargeback rates. These factors suggest higher liability for acquiring banks, which is why they cause deeper scrutiny.

To better understand why your business may be labeled “high-risk”, consider the standard contributing factors used across the payments industry. If your business comes under below criteria then your business comes under a high-risk classification:

- If your monthly sales volume is $20000 or more: Higher volume increases potential chargeback exposure.

- Whether you accept multiple currencies or process cross-border transactions: International sales often carry higher fraud and refund rates.

- Whether your average ticket size is $500 or more: High-ticket transactions are more likely to be disputed and more costly when reversed.

- Whether you offer recurring billing or subscription payments: Subscriptions often generate disputes because of renewal confusion or forgotten charges.

- Whether you have a history of high chargeback volumes: Anything above 1% per card-network rules raises red flags.

- Whether you sell intangible products: such as digital goods, SaaS, downloadable content, or even tickets. These items usually have higher refund and fraud rates because they cannot be physically proven or returned.

- If you operate in chargeback-prone regions: outside the U.S., EU, Canada, Japan, or Australia. Certain countries are associated with increased fraud activity.

It’s important to understand that being designated as a high-risk merchant does not make your business untrustworthy, nor does it reflect on the quality of your products or your professional reputation.

Instead, this classification is a subjective risk assessment used by payment service providers to estimate the chances of disputes, fraud, or regulatory complications related to your industry or operating model.

Ultimately, being labeled high-risk simply means your business requires a specialized merchant account structure with improved oversight. In many cases, it is the only compliant way to continue accepting card payments securely and sustainably especially if you operate in a rapidly evolving or regulated market.

Also Read: Contractor Payment Solution

Can I Get a High-Risk Merchant Account With Instant Approval?

Many business owners search for instant approval of high-risk merchant accounts hoping to start accepting payments immediately.

Although the promise of instant approval is attractive particularly for merchants previously declined by major processors, the truth is that no reputable provider can offer genuine, same-moment approval for a high-risk merchant account.

Usually high-risk business owners search for fast approval, and not instant approval because federal regulations make real instant onboarding impossible.

High-risk merchants operate in industries with increased financial exposure, regulatory scrutiny, and chargeback sensitivity. Due to this, acquiring banks must conduct additional underwriting to verify the business model, product legality, website compliance, refund policy, financial stability, and risk profile of the merchant.

Low-risk sectors like retail shops, salons, professional services, or simple e-commerce stores often pass underwriting quickly because they have minimal liability and rarely deal with regulatory oversight.

High-risk merchants, however, operate in categories such as CBD, Kratom, nutraceuticals, coaching, subscription models, firearm accessories, travel or dropshipping.

These industries require enhanced due diligence(EDD). Banks must review documents like COAs, supplier information, fulfillment timelines, age-verification systems, and processing history to ensure compliance with card-network rules and federal laws.

Having said that, fast approval is absolutely achievable often within 24 to 48 hours and if merchants provide complete documentation and maintain a fully compliant website. Also streamlining underwriting to reduce friction, accelerate onboarding, and help high-risk businesses go live as quickly as legally possible.

How Long Does It Take for High-Risk Merchant Account Approval?

The approval timeline for a high-risk merchant account is longer than for standard, low-risk accounts because banks must perform deeper due diligence.

On average, high-risk merchant accounts take three to five business days to receive final approval. This extended timeframe is necessary because underwriters need to carefully evaluate the credit history of the business, chargeback patterns, financial stability, product category, and overall regulatory exposure.

However the process does not have to feel slow or uncertain. They usually look for merchant account providers who specialize in streamlining high-risk onboarding and can typically issue a pre-approval within 24 hours.

Such pre-approval is a major first step, allowing you to begin assembling your file and preparing it for bank-level underwriting. Once pre-approved, your application will be forwarded to acquiring bank partners for their final review.

Before we work closely with banks that understand high-risk industries, it can often expedite final approval, ensuring the fastest turnaround possible. The more prepared a merchant is, the more quickly the approval process tends to move.

To keep your approval moving smoothly, make sure you submit every required document and detail promptly and in full. Missing paperwork , delayed responses are some of the most common reasons why high-risk approvals take longer than expected.

By staying organized and responsive, you can shorten the process and begin processing payments sooner.

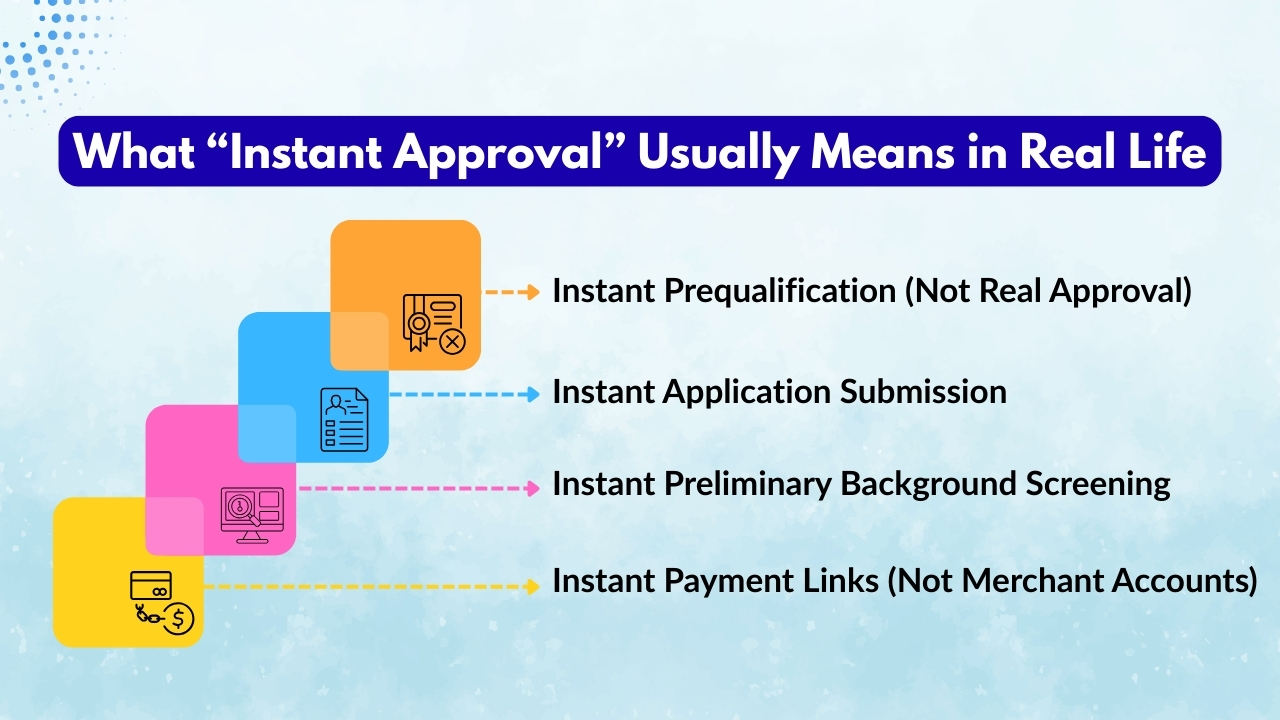

What “Instant Approval” Usually Means in Real Life

When a payment processor claims to offer instant approval for high-risk merchant accounts, it hardly means true merchant account approval. Rather most companies use the term to describe a faster onboarding experience without actually bypassing underwriting, compliance checks, or bank verification. Here’s what “instant approval” typically refers to:

1. Instant Prequalification (Not Real Approval):

It is simply a quick screening to confirm whether your industry is supported. You submit basic details, and the system instantly tells you whether you may qualify. However, the bank has not reviewed your products, documents, or compliance, so this is not a real approval.

2. Instant Application Submission:

Merchants can often fill out an online form and upload documents within minutes. Though the document submission is instant, underwriting still takes 24-72 hours because banks must perform KYC, AML checks, and review your website.

3. Instant Preliminary Background Screening:

Some processors run automated checks such as identity verification, business lookups, website scans, OFAC screening within seconds. Such tools streamline the process but do not replace full underwriting.

4. Instant Payment Links (Not Merchant Accounts):

Some platforms give temporary payment links immediately but these are risky. They are often not allowed for high-risk industries but may cause account shutdowns and can lead to frozen funds or account termination.

How to Choose the Right High-Risk Payment Processor

Selecting the right high-risk payment processor is one of the most strategic decisions that a business can make. High-risk merchants face stricter underwriting requirements, higher fees, and more regulatory oversight than low-risk merchants.

Due to this, your payment processor must be more than just a service provider; rather, it must be a knowledgeable partner who understands your industry, supports compliance, reduces risk, and provides long-term stability.

Whether you operate in CBD, Kratom, nutraceuticals, travel, coaching, subscription billing, dropshipping, credit repair, firearms accessories, or any other regulated or chargeback-prone vertical , the right processor can determine how smoothly your business runs.

Below are some of the most important factors to consider when selecting a high-risk payment processor.

1. Experience With High-Risk Industries:

The most important requirement is selecting a processor with direct experience in high-risk verticals. High-risk payment processing is significantly more complex than low-risk processing, so just a generalist provider will not understand the regulatory challenges, underwriting expectations, or industry-specific risks associated with your business model.

A processor experienced in your industry will:

- Understand the legal landscape

- Know which acquiring banks accept your product type

- Advise on website and marketing compliance

- Identify risk patterns specific to your vertical

- Provide customized risk-mitigation strategies

- Help prevent unnecessary account shutdowns.

For instance, CBD and Kratom require COAs and THC limits; adult merchants need age verification; coaching requires clear refund policies; and supplements need proper labeling. Only a processor familiar with your vertical will ensure approval and long-term stability.

2. Risk Management and Fraud Prevention:

High-risk businesses usually have higher chances of fraud, friendly fraud, and chargebacks. Due to this it is essential for your processor to offer strong risk-management tools to protect your revenue and keep your chargeback ratio below acceptable limits.

Look for processors that provide:

- Real-time transaction monitoring

- Advanced fraud scoring

- Chargeback alerts and mitigation services

- 3D Secure (3DS2) authentication

- Address Verification Service(AVS)

- Velocity checks for limits on frequency or amount

- Blacklist and whitelist controls

- AI-powered fraud detection models

Fraud prevention is not optional in high-risk processing. A strong risk-management system reduces chargebacks, preserves your merchant account, and protects your business reputation.

3. Multiple Payment Options:

In today’s global market, customers expect to pay the way they prefer. High-risk businesses often face limitations with card payments alone, so offering multiple payment options increases conversions and ensures continuity even if one method experiences downtime.

Your processor should support:

- Credit or debit cards

- ACH/eCheck

- Bank transfers or wire transfers

- Digital wallets

- Buy Now, Pay Later(BNPL) options

- Payment links and invoicing

- Crypto payments

- Alternative payments like SEPA, iDEAL, Klarna, GCash and more.

The more payment methods your processor supports, the higher your revenue and customer satisfaction.

Also Read: Restaurant Credit Card Processing

4. Competitive Fee Structure:

High-risk merchant accounts naturally incur higher fees because of greater financial liability for banks and processors. Yet, you should ensure your processor offers transparent pricing and a fair fee structure.

Evaluate:

- Processing rates

- Chargeback fees

- Monthly fees

- Rolling reserve requirements

- Payout cycles

- International transaction fees

- Refund or return fees

- Monthly minimums

- Gateway fees

Typical high-risk rates includes:

- 3.5% – 7.5% for processing

- 5% – 10% rolling reserve

- 3 – 7 day payout schedule

Ensure your processor clearly explains all fees upfront. Avoid companies which hide fees, lock you into long-term contracts without flexibility, or seem too cheap to be legitimate which are often warnings.

5. KYC & Regulatory Compliance Support:

High-risk industries often carry heavy compliance requirements. Whether it’s COA documentation for CBD, age verification for vape shops, labeling rules for supplements, or AML or KYC regulations for financial services, your processor must support you in staying compliant.

Strong processors provide:

- Website compliance audits

- Product and SKU approval guidance

- Age verification tools

- COA and lab report validation

- FTC or FDA advertising compliance guidance

- PCI DSS compliance tools

- Fraud-prevention best practices

- Chargeback monitoring and reporting

A processor which understands your industry’s regulations reduces your risk of account termination, frozen funds, or legal complications.

6. Excellent Customer Support

In the high-risk world, issues like payment declines, sudden chargeback increases, gateway errors, and compliance questions must be addressed quickly. That’s why excellent customer support is essential.

A good processor will offer:

- Fast response times

- Knowledgeable support staff

- A dedicated account manager

- Integration and technical support

- Billing support and reconciliation assistance

- Proactive communication.

When your business depends on revenue flow, reliable support can make the difference between smooth operations and costly downtime.

Also Read: Hospitality Merchant Services for Hotels and Resorts

7. Scalability and Growth Prospects:

Your payment processor should scale with your business as you grow. If you plan to increase transaction volume, expand internationally, launch new products, or open additional merchant accounts, your processor must be able to support that growth.

Look for:

- Support for high processing volumes

- Multi-currency capabilities

- Global acquiring bank partners

- Tiered pricing as volume increases

- Additional merchant account options

- Smart payment routing

- APIs for custom development

- Marketplace or multi-vendor support

A scalable processor ensures your payment system remains stable even as demand increases.

8. Reputation and Reviews:

In the high-risk arena, reputation is everything. Before choosing a processor, research its history thoroughly. Before choosing a processor, research its history thoroughly.

Check:

- Google reviews and ratings

- Trustpilot and BBB listings

- Industry backgrounds

- Testimonials from similar high-risk merchants

- Case studies

- LinkedIn company history

- Longevity in the high-risk space

- Acquiring bank relationships

Warning signs include:

- Complaints about withheld funds

- Unclear contract terms

- Promises of “instant approval”

- No visible leadership team

- Limited online presence

- Hidden fees

A processor’s track record will reveal whether they are trustworthy or likely to create problems.

9. Integration and Compatibility:

Smooth integration ensures quick deployment and reduces operational friction. Your processor should integrate smoothly and effortlessly with your existing technology stack, including:

eCommerce Platforms:

- Shopify

- WooCommerce

- Magento

- BigCommerce

- PrestaShop

- OpenCart

Membership and CRM Platforms:

- ClickFunnels

- Kajabi

- Kartra

- Keap/Infusionsoft

- ThriveCart

POS Systems:

For retail or hybrid businesses.

Custom APIs:

For SaaS, fintech, apps, custom software, and marketplaces.

Recurring Billing Support:

For subscription-based businesses. Compatibility saves development time, reduces integration errors and also supports fast onboarding.

Also Read: Retail Payment Platforms

How Fast Approval Really Works (24–48 Hours)

Legitimate high-risk processors still perform full due diligence, but they optimize the steps so you can start processing quickly, usually achieving fast approval within 24-48 hours once all required documents are correctly submitted.Here’s how that process typically works:

1. Smart Application Intake:

You start by completing an online application with key business details like legal name, industry type, website URL, expected processing volume, average ticket size, and product category. The more accurate and transparent you are at this stage, the fewer follow-up questions and delays you will face later.

2. KYC (Know Your Customer) Verification:

The next step is the bank or processor validates the identity of the business owner and entity. They review your government-issued ID, business registration documents, EIN, and sometimes proof of address. This step ensures they know exactly who they are working with and that the entity is legitimate.

3. Detailed Underwriting Review:

Underwriters then assess your risk profile. They look at what you sell, where you source it from, your shipping methods, supplier credentials, refund and cancellation policies, subscription billing practices, and past chargeback history if you have processed elsewhere. This is where most high-risk evaluation happens.

4. Website & Compliance Audit:

Your website is reviewed to confirm it meets card brand, regulatory, and industry standards. They check for prohibited medical claims (especially for CBD and supplements), age verification where required (vape, adult, kratom), clear terms and policies, COAs for CBD, and accurate labeling and disclosures.

5. Final Approval & Account Activation:

If everything checks out, your account is approved and activated—often within 1 to 4 business days, and in many cases 24–48 hours. You then receive your gateway credentials, integration details, and can begin processing payments with a stable, compliant high-risk merchant account.

Also Read: Smart Payment Solutions for Gaming and Esports

How Risk Levels Affect Approval Speed

In high-risk payment processing, your industry category directly influences how fast your merchant account can be approved. The higher the perceived risk due to regulations, chargebacks, or reputation, the more time underwriters need to review your business, products, and website.

1. Fastest Approval Industries (24–48 Hours):

Service-based and informational businesses such as consulting, coaching, digital marketing, and low-ticket subscriptions usually see the quickest approvals. They tend to have lower chargeback risk, simpler products, and fewer legal restrictions, so underwriting can move quickly once documents and website compliance are in order.

2. Moderate Approval Timeline (2–4 Days):

Industries like CBD topicals, nutraceuticals, drop shipping, and beauty products require more scrutiny. Banks need to review ingredients, fulfillment methods, and refund policies to ensure products are safe, legal, and delivered as promised.

3. Slower Approval Industries (4–10 Days):

The slowest approvals are usually seen with CBD ingestibles, kratom, vape products, adult content, high-ticket coaching, travel, and stimulatory supplements. These carry higher regulatory, reputational, or chargeback risk.

Underwriters must evaluate compliance, age restrictions, marketing claims, and historical disputes more carefully, which naturally extends the approval timeline.

How to Increase Your Chances of Approval

Getting approved for a high-risk merchant account is all about making your business look organized, transparent, and compliant. The more confidence you give underwriters, the faster and smoother your approval.

1. Have All Documents Ready:

Before you even apply, collect everything you know the processor will ask for such as business registration documents, EIN letter, owner ID, bank statements, processing history, while if you are in CBD or supplements you will require up-to-date COAs or basic business paperwork forces underwriters to chase you for information, slows the process, and can make you look unprepared or disorganized.

2. Fix Website Compliance Issues:

Your website is one of the first things underwriters check. Many rejections happen simply because of incomplete refund policies, missing terms, unclear or absent contact details, medical claims, or missing COA links.

Add clear refund, privacy, terms, and shipping pages, display a real address or email or phone, and remove disease or cure-type claims. A clean, professional, compliant website instantly improves your credibility.

3. Be Transparent About Suppliers:

Banks want to know exactly where your products come from and how they are produced. Be open about your manufacturers, labs, and raw material sources. Share licenses, testing standards, and certifications when available.

Transparent supply chains suggest long-term stability, while unclear or secretive sourcing can look risky and cause underwriters to hesitate or decline.

4. Reduce Chargebacks Before Applying:

If your previous processor shows a high dispute or chargeback ratio, address that first. Improve order tracking, clarify billing descriptors, strengthen customer support, and manage expectations on your sales pages.

Showing that you have actively reduced chargebacks proves you are committed to sustainable and compliant processing.

5. Avoid Misleading Marketing:

Overpromising is one of the fastest ways to raise red flags. Exaggerated results, guaranteed income, miracle cure, or unrealistic promises make both banks and regulators nervous.

Use honest, balanced messaging with realistic benefits, proper disclaimers, and no hype. The more grounded and accurate your marketing, the safer you appear to an underwriter.

Conclusion

Securing a high-risk merchant account with so-called “instant approval” is often more marketing language than reality but it does not mean you are stuck waiting weeks to start processing.

The key is understanding how banks actually evaluate risk and place your business so you look as clean, organized, and compliant as possible.

In highly regulated industries like CBD, Kratom, supplements, adult, vape, travel, high-ticket coaching, and subscription models, processors simply cannot skip KYC, AML checks, and underwriting.

Those steps are not optional; rather they are required by law and by the card networks. Any provider claiming to bypass that is either being misleading or is putting you at risk of frozen funds, sudden shutdowns, and reputational damage.

While the good fact is that fast approval is absolutely real. If you have your documents ready, a well polished and compliant website, your supply chain transparent, and your chargeback history under control, many high-risk processors can approve you within 24-48 hours and get you live within a few business days.

Ultimately, your goal is not just to get an account rather to keep it. It means choosing a processor which actually understands your vertical, being honest about what you sell, investing in good customer service, and maintaining compliance over the long term.When you treat payment processing as a long-term partnership instead of a shortcut, you lower risk for both your business and the processor.

So instead of chasing instant approval promises, focus on what serious underwriters care about such as documentation, transparency, compliance, and realistic marketing. By doing all the requisite processes, you won’t just get approved faster rather you will be building a payment foundation which your business can safely scale on.

If you still have any query regarding high-risk merchant account instant approval then feel free to write to us at Ace Merchant processing and we are more than happy to assist you.