Running a restaurant today requires mastering great food, great hospitality, and great payments. This guide explains restaurant credit card processing and why selecting the right tools matters.

Make your POS and gateway work together to accept chip, tap, Apple Pay, Google Pay, and QR code payments so checkout stays fast and easy. Tableside payments with handheld terminals speed up service and boost tips.

Security is non-negotiable so it is essential to follow PCI compliance, keep PAN out of scope with tokenization, and secure devices with point-to-point encryption(E2EE).

Enforce least-privilege, role-based access, patch often, and log access. For omnichannel restaurants, adopting a cross-channel token lets guests save a card once and reuse it for tabs, preorders, memberships, and rewards without your systems even storing PANs.

Lower costs by optimizing interchange sending Level ll/lll data when eligible, and where lawful using compliant surcharging, dual pricing, or cash-discount programs that meet card-brand and local requirements. Prioritize fee transparency with statements that clearly separate interchange, assessments, processor markups, and gateway fees to avoid surprises.

Ensure operational essentials are built in like tip adjustments, pre-auths, bar tabs, partial captures, reliable batch close, and quick voids or refunds. For delivery and takeout, use saved cards with network tokens plus AVS, CVV, device fingerprinting, and 3-D Secure to reduce chargebacks while keeping approvals high.

Select a processor that offers next-day payouts, strong dispute support and a ledger that reconciles authorizations, settlements, chargebacks, and fees. Choose a platform which has high approval rates, multi-acquirer routing, offline mode for outages, and round-the-clock support. Combine a restaurant merchant account with tight POS integration and disciplined processes in order to make payments invisible to guests while increasing approvals, lowering costs, and safeguarding margins.

Also Read: What is Payment Processing Software

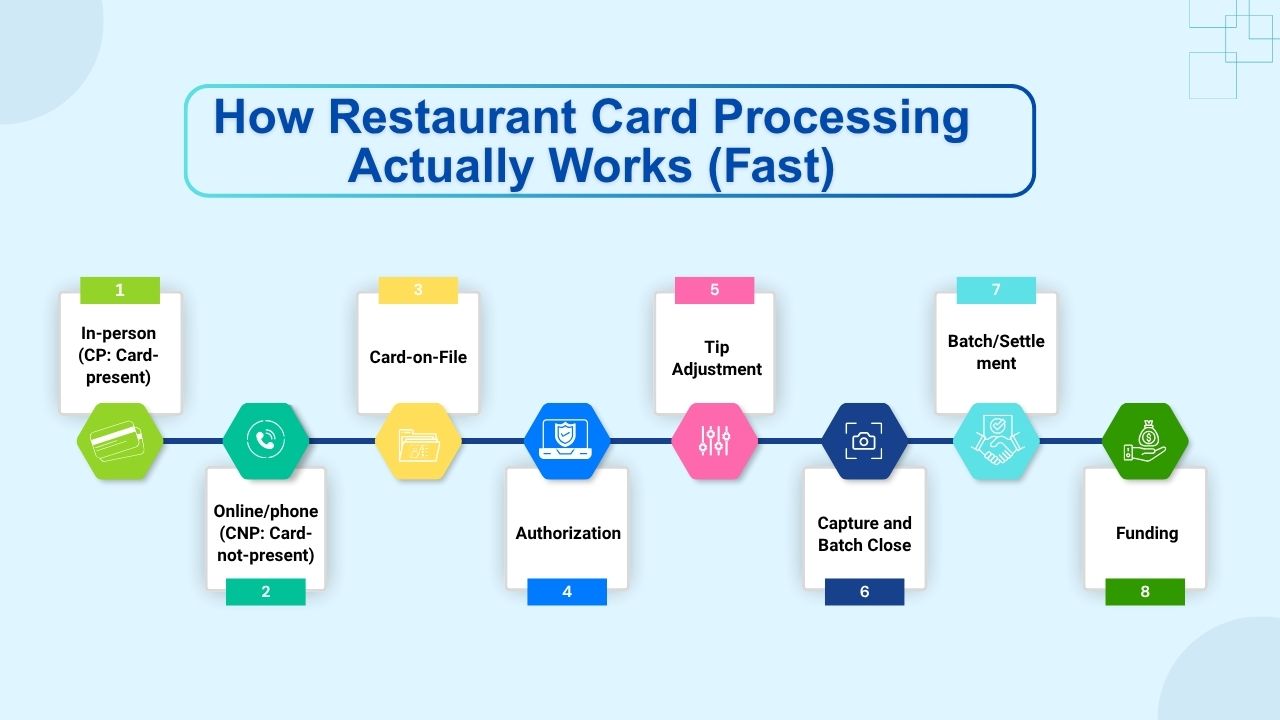

How Restaurant Card Processing Actually Works (Fast)

Day to day, restaurant payments run through three channels which are card-present in person, card-not-present online or by phone, and card-on-file for tabs and subscriptions.

1. In-person(CP: Card-Present):

Card-present payments use EMV chip dips, contactless NFC taps, contactless NFC taps, or magstripe fallback on counters, bars, handhelds, and pay-at-table devices, delivering faster approvals, lower fraud, higher tip capture, and fewer issues than online or keyed transactions.

2. Online/phone(CNP: Card-Not-Present):

Card-not-present includes takeout sites, marketplaces, QR-to-web ordering, and phone payments keyed into a virtual terminal, with higher fraud risk and costs than card-present, requiring AVS, CVV, 3-D Secure, velocity limits, clear descriptors, and delivery proof.

Also Read: Smart POS System

3. Card-on-File:

Card-on-file uses tokenization to save cards securely for bar tabs, order-ahead pickups, subscriptions like wine clubs or chef’s tables, and catering deposits and final charges, reducing PCI scope, speeding checkout, and improving rates and tips.

Behind the scenes, every transaction follows the same route from authorization to tip adjustment, capture, batch settlement, and final funding.

Also Read: Top 5 Features Retailer Should Look into Modern Terminal

4. Authorization:

Payment starts when the terminal reads the card via EMV chip, contactless NFC or a manual keyed fallback. Your POS or handheld encrypts the data and sends it to the gateway or processor which routes it through the card network to the issuing bank. The issuer checks funds, risk, and fraud signals, then replies with approve or decline and an auth code usually in below two seconds. Bars and full-service restaurants often preauthorize a small amount, like $1 or the subtotal, to keep tabs open.

5. Tip Adjustment:

Restaurants usually preauthorize the check amount, then add the tip afterward once the guest signs or choose a tip on the device. Counter service captures tips at the device during checkout.

Table service usually adds the tip after the guest signs or selects on a pay-at-table device. The POS performs a tip adjustment against the existing authorization with no new card entry required.

Also Read: The Future of Retail Payments

6. Capture and batch close:

Approvals are only reservations until you capture them. Most restaurants usually run an automatic batch usually at the end of service. The batch groups all captured transactions and sends them to the networks for settlement. Clean batching without open tabs or orphaned authorizations prevents mismatches and funding delays.

7. Batch/Settlement:

At the end of the day, or on an auto-batch, approved authorizations are captured, grouped into a batch, and transmitted to the acquirer and card networks for settlement which initiates funding to the merchant account and updates transactions for reconciliation and reporting.

8. Funding:

Depending on your provider, deposits arrive the next day or T+2, or sometimes the same day, landing in your bank either net of fees or as gross settlements with fees billed monthly, and accompanied by reports that reconcile settled batches to transactions.

Fast, reliable authorizations and clean batching are the biggest levers for approvals, tips, and cash flow.

Also Read: How Retail Payment Methods Transforming the Market

Pricing Models, Fees, and What a “Good” Effective Rate Looks Like

1. Interchange-Plus(IC+):

Such pricing passes through the actual network costs interchange fees set by card networks and assessment fees, then adds a fixed, transparent markup, often expressed as a percentage plus per transaction fee. As the processor’s margin is clearly separated from the non-negotiable network fees, merchants gain visibility into true costs. While it may look more complex than flat-rate models, IC+ is widely regarded as the fairest and most cost-effective option for merchants processing significant volumes offering scalability and transparency.

2. Flat-Rate:

Flat-rate keeps costs simple with a single blended fee per channel for instance, 2.6% + $0.10 at the counter and 2.9% + $0.30 for online orders. It’s budget friendly to predict and simple to reconcile since interchange and assessments are already built into the rate. Your trade simplicity for efficiency like large volumes often see higher effective rates than IC+, notably on debit. Additional charges can apply like keyed-in surcharges, cross-border fees, and chargeback fees among them. Flat-rate suits small or inconsistent volumes, but while your business grows, the missing cost granularity can increase your total processing spend higher.

3. Tiered or Bundled:

Tiered or bundled models classify transactions into Qualified, Mid-Qualified, and Non-Qualitified buckets where each priced differently. Though it is marketed as easy, yet opaque rules that can change obstruct clean statement reviews. Low-risk debit may downgrade due to rewards, card-not-present, or AVS or settlement quirks, inflating costs. Extra surcharges and non-equal downgrades often hide costs that would be lower on Interchange-Plus. When the transaction mix shifts, effective rates often inch upward.

Common fees you will encounter:

1. Interchange:

Interchange is the fee paid to the issuing bank of the cardholder that varies by card type, rewards level, and whether the transaction is card-present or card-not present, directly impacting merchant processing costs.

2. Assessments:

Assessments are mandatory fees charged by card networks such as Visa and Mastercard. It is a small percentage of total transaction volume, applied uniformly across all sales, regardless of card type, processor, or rewards program.

3. Processor markup:

It represents your payment provider’s profit margin. Processor markup combines a small percentage of transaction volume with a fixed per-transaction fee, covering the processor’s operational costs and revenue.

4. Monthly:

Monthly fees often include an account maintenance charge, PCI compliance program cost, and statement delivery fee. Some providers may also include a gateway fee if you use an online payment processor.

5. Hardware:

Hardware costs include purchasing or renting payment terminals and handheld devices. Providers may also charge for service plans which includes maintenance, updates, and support and thereby ensuring reliable performance and compliance with security standards.

6. Chargeback:

A chargeback occurs when a customer disputes a transaction, and processors impose a per-case fee applied whether you win or lose the dispute, adding to operational and financial burdens for merchants.

Also Read: Retail Payment Methods

7. Early termination:

Early termination fees punish you for canceling a processing agreement before its term. So avoid contracts with ETFs; negotiate month-to-month terms or no-penalty terms exists to maintain flexibility and use leverage when needed.

8. Effective rate:

Your actual processing cost is calculated by dividing total fees by total card volume. So restaurants usually aim for an overall effective rate of 2.2% – 2.9%, on the basis of card-present versus card-not-present transactions and card types. However, heavy online ordering, higher AmEx share, or small-ticket sales can raise the effective rate beyond the target.

9. Watchouts

- Hidden non-qualified tiers or unexplained downgrades increase costs, concealing true pricing and making monthly statements confusing and hard to audit.

- Different small fees like PCI, regulatory, compliance, batch, AVS, gateway add up and push your effective rate higher.

- Confirm whether American Express is billed pass through at true interchange or blended into a higher rate; this setting changes your effective rate, especially with high Amex volume or small-ticket averages.

- Per-transaction adders: Some flat-rate providers quietly apply per-transaction adders like AVS checks, gateway usage, or risk surcharges which are layered above the promised rate, pushing overall processing costs higher than that merchants accept.

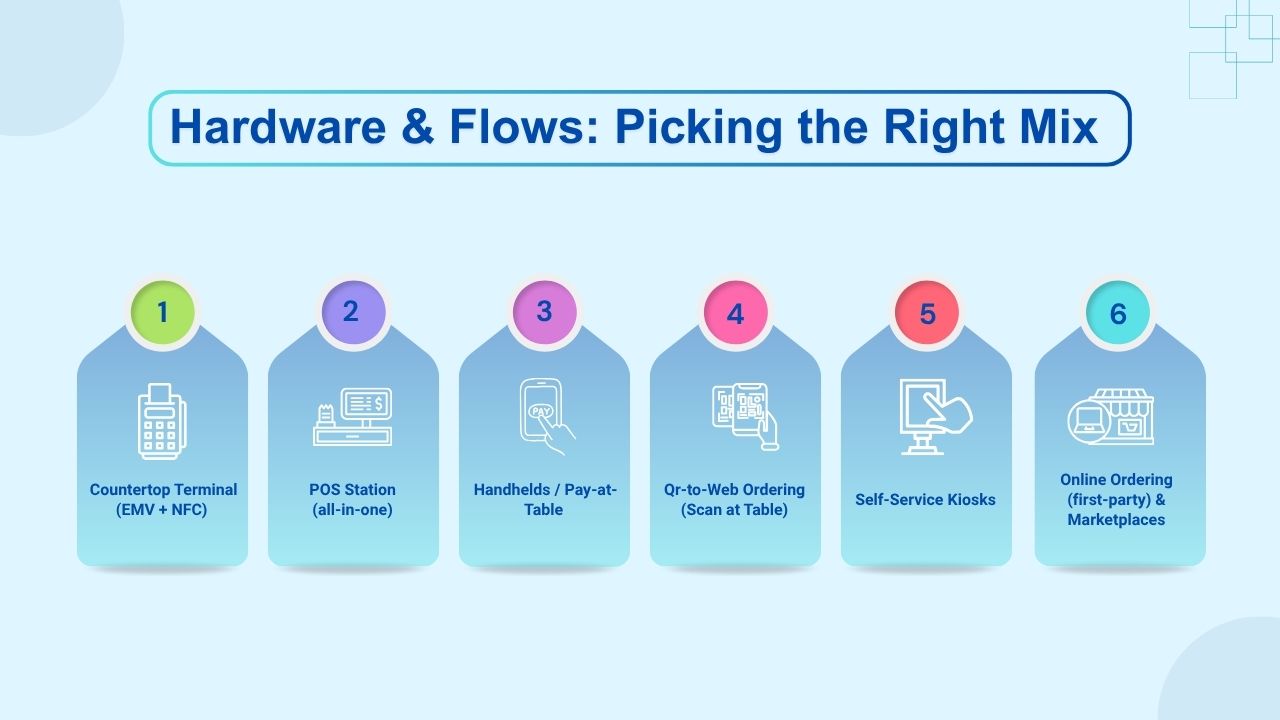

Hardware & Flows: Picking the Right Mix

1. Countertop terminal (EMV + NFC):

Use: A countertop terminal with EMV chip and NFC tap supports fast, secure checkouts; which is ideal for counter service, coffee bars, bakeries, and quick-serve concepts where speed, reliability and simple workflows matter.

Pros: Countertop EMV or NFC terminals are inexpensive, quick, and easy to operate with minimal setup and training. Because of their small footprint frees up space making them ideal for cafes, bakeries, and quick-serve environments.

Cons: Tip options are limited with basic prompts, table-service tipping feels awkward, scaling lines requires more cabled devices, mobility is constrained, and splitting checks or modifiers is badly executed without an integrated POS.

2. POS Station (all-in-one):

Use: A POS station(all-in-one) is designed for full-service dining, bars, and busy QSRs, supporting kitchen routing, table management, modifiers, coursing, split checks, advanced tipping, and integration with printers, cash drawers, and other peripherals.

Pros: A unified POS links menus, modifiers, table maps, KDS, printers, online ordering, loyalty, gift cards, reporting, inventory, purchasing, labor, timecards, and permissions which makes operations smooth, reducing errors, and syncing FOH, kitchen, and bar.

Cons: All-in-one POS stations come with higher upfront and ongoing costs, that require migration effort when switching systems, and demand staff training time to learn new workflows, features, and integrated hardware or software components.

3. Handhelds / Pay-at-Table:

Use: Handheld pay-at-table devices suit full-service dining, patios, bars, and fast-casual curbside. It enables tableside ordering, EMV or NFC payments, faster turns, on-screen tip prompts, fewer walk-aways , smoother service, and easier check splits with routing to kitchen or bar.

Pros: Handheld pay-at-table devices accelerate service and table turns, lift tips through on-device prompts, minimize card handoffs, cut walk-outs, and let servers split checks at the table improving accuracy, guest satisfaction, and peak-hour throughput and revenue overall.

Cons: Handheld rollouts add device provisioning and charging logistics, requiring dependable Wi-Fi or LTE coverage across patios and dead zones, and demand staff training to master workflows, troubleshoot connectivity issues and maintain speed and guest experience.

4. QR-to-Web Ordering (scan at table):

Use: QR-to-web ordering allows guests to scan a code at the table to browse menus, order, and pay on their phones. It is ideal for fast-casual restaurants, breweries, and food halls who are aiming to smooth service, improve efficiency, and reduce wait times.

Pros: Fewer servers are required, enables guests control pacing and choices, built-in upsell prompts which increase check size, and one-tap reorders speed rounds improving labor efficiency, reducing wait times, and improving peak service across fast-casual brewery, and food hall operations.

Cons: It includes guests who prefer human interaction, depending on charged devices and stable Wi-Fi, and the need for a clear menu UX; confusing flows, slow networks, or dead batteries that can obstruct orders and frustrate diners.

5. Self-Service Kiosks:

Use: Self-service kiosks are ideal for Quick Service Restaurants(QSRs), busy lunch spots, and food courts. Guests browse menus, customize orders, and pay directly on the screen. It reduces lines, improving order accuracy, enabling upsells, and freeing staff to focus on preparation and fulfillment during peak demand.

Pros: Self-service kiosks manage big queues effectively, keeping throughput smooth during peak hours. Being built-in prompts encourage consistent upsells, improving check sizes. Due to clear digital menus helps to reduce order-taking errors, improving accuracy, while freeing staff from registers to focus on food preparation, fulfillment, and faster service overall.

Cons: Kiosks add upfront hardware expenses and ongoing maintenance, demand floor space for stands or wall mounts, and require frequent cleaning of touchscreens. Accessibility must be addressed like height, reach, contrast, screen readers otherwise you risk excluding guests and slowing service when queues form around the devices during peaks.

Also Read: Retail Payment Platform

6. Online Ordering (first-party) & Marketplaces:

Use: Takeout, curbside, delivery. Combine first-party ordering with marketplaces to collect takeout, curbside, and delivery demand. Keep brand control and data on your site, while marketplaces drive discovery, overflow capacity, and new neighborhoods efficiently.

Pros: New revenue streams like prepayment and order-ahead options unlock additional income by extending sales opportunities beyond in-store traffic and creating a smoother, more consistent revenue flow.

Prepaid orders improve cash flow, reduce customer no-shows, and ensure more predictable revenue by securing payment upfront before the service or product is delivered.

Ordering ahead smooths kitchen load, shortens queues, balances peak hour pressure, and improves throughput. Digital channels allow upsells, personalized offers, and data collection for marketing.

Cons: Higher card-not-present(CNP) fees, complex delivery logistics, and additional marketplace commissions which can impact overall profits.

Tipping Flows and Service Charges Without Drama

1. Counter service:

For courier service, tip prompts should appear after payment is initiated, providing balanced options like 10%, 15%, or 18%, and a “No tip” button to ensure fairness and customer comfort.

2. Full service:

Preauthorize the base amount, then present a server handheld or pay-at-table flow with clear, fair tip options like 15%, 18%, or 20% and custom reducing friction, preventing surprises, accelerating checkout, and improving staff satisfaction.

3. Delivery:

Display tip options before checkout to set expectations and reduce friction; after delivery, re-prompt post delivery via SMS or email receipt with one-tap amounts and custom entry, reinforcing trust and improving conversions.

4. Service charges and fees:

Service charge for instance 18% large party fee is different from a surcharge on card payments. They are not interchangeable. If you use service charges, then it is essential to label them clearly and train staff on how to explain them.

Ensure tax calculation handles them correctly and tips are not wrongly taxed or double-charged depending on your jurisdiction rules.

5. Tip pooling and reporting:

Select a POS that exports card tips by server, supports pooling rules, and delivers clean payroll reports like tip declarations, cash versus card breakdowns, and automatic calculations.

Security and Compliance: PCI, Tokenization, P2PE/E2EE

1. Goals:

Keep raw PAN(card numbers) off your systems by posting card data directly to PCI certified endpoints. Encrypt end-to-end from the capture to processor using E2EE or P2PE.

Tokenize immediately so saved cards, tabs, and recurring payments reference tokens, not PAN, shrinking PCI scope, breach exposure, and audit overhead.

2. What to implement:

- Hosted or embedded fields : Enable hosted or embedded fields for online ordering so the browser posts card data directly to PCI-certified endpoints.

- Point-to-Point Encryption (P2PE): Deploy P2PE-capable terminals and handhelds so card data encrypts at swipe, dip, or tap and stays protected end-to-end, reducing PCI scope, liability, and audit burden.

- Role-based access and least-privilege : Enable Role-based access and least privilege is POS and reporting tools, granting necessary permissions, auditing logs, and revoking unused accounts to reduce fraud risk, limit data exposure, and ensure compliance.

- Short data retention: Set short retention windows for stored card tokens, enable automatic removal of inactive records, reduce exposure and PCI scope, simplify audits, and prevent sensitive payment data from accumulating across systems.

- Regular SAQ: Complete the appropriate PCI SAQ regularly and train staff on security basics like phishing, device handling, data hygiene and strictly forbid writing card numbers on paper or screenshots.

3. Incident readiness:

Signed webhooks and structured logs with correlation IDs help trace issues.

A simple playbook for device theft/loss, suspected skimmers, or suspicious refunds: who to call, how to revoke device keys, how to rekey terminals.

Fraud, Disputes, and Chargebacks: A Restaurant-Ready Playbook

Common restaurant chargeback happens because of:

- walk-outs or claims of “I never dined there” from stolen card use.

- delivery or takeout disputes like “never arrived” or “not what I ordered” and high-ticket catering deposits or event no-shows where cancellation terms are unclear, signatures missing or proof of weak delivery.

Prevention tactics

- For dine-in: Adopt EMV and contactless with chip cryptograms, pay-at-table flows, and guided device prompts to reduce manual key-entry, reduce fraud, speed checkout, and reduce PCI scope. Keep signed itemized receipts like paper or digitals. For tabs, capture and store an authorized token and ID verification when appropriate.

- For takeout/delivery: Obtain address/phone verification in the order flow; use order confirmation and delivery proof (photo, driver app logs, signed receipt). Offer secure order-ahead with verified accounts.

- For catering/events: Use e-sign agreements with clear terms (cancellation limits, damage clauses), split deposits, and collect a card on file token.

When a dispute hits

- It is essential to act fast as deadlines are real.

- Submit itemized receipt, EMV/terminal proof (AID, TVR, TSI, CVM), order logs, delivery evidence, and any guest communication.

- Keep an organized folder system by date, reason code, case number. Your win rate increases when evidence is complete and consistent.

Funding, Batching, Reconciliation, and Month-End Close

1. Batching & funding

- Auto-batch daily at a consistent time for faster funding and reconcile tips. Many restaurants close batches after the last seating or kitchen closes.

- Clarify funding schedule like next-day versus T+2 versus same-day. For holidays ask your provider for a holiday aware payout calendar so you get to exactly know when funds hit.

2. Reconciliation

Your ideal flow:

- Run a POS Z-read (end-of-day) report showing gross sales, comps, voids, discounts, service charges, and tips.

- Run a payment batch report showing authorization counts, captured transactions, and tip adjustments.

- Run a processor deposit report showing gross deposits, fees deducted, and net payout.

- Enable an accounting bridge to QuickBooks or Xero that maps tenders (Visa, Mastercard, Amex), gift cards, and house accounts to the correct ledger accounts for clean reconciliation.

- Keep daily variance at $0.00. If not, review open tabs, post-batch voids, offline authorizations, and manual refunds.

3. Refunds & partials

Train supervisors on partial refunds and tip-safe reversals, and apply T+1 refund holds to high-risk orders where policy permits.

Optimization: Routing, Approvals, Speed, and Guest Experience

1. Authorization rates:

Approvals drive revenue. Focus on:

- Clean data: Validate inputs at capture like full ZIP or AVS when required, correct expiry, normalized address or country formats, and complete, consistent customer identifiers. Reject truncated ZIPs, expired cards, and mismatched fields.

- Network tokens: Store cards as network tokens (e.g., Visa/Mastercard tokenization) so PAN updates flow automatically on reissue, cryptograms bind device/channel, and approval rates rise while PCI exposure falls.

- Smart retries with idempotency: Classify declines (soft vs hard), back off smartly, honor issuer retry-after hints, rotate credentials if required, and attach idempotency keys so retried requests can’t double-charge. Log retries for audit.

2. Speed at service:

- Tap to pay: NFC or contactless reduces checkout to seconds, reducing errors and wait time. One-tap tipping increases tip capture, digital receipts clear terminals faster improving throughput at rush, bars, and curbside pickup.

- Server handhelds: Tableside ordering and payment reduce trips to the POS, remove re-keying, saving minutes per turn. Split checks, menu updates, and pay-at-table reduce errors, speed service, and lift covers.

3. Upsell without pressure:

Digital flows like handheld, QR, kiosk, and online. It should surface tasteful add-ons like extra sides, sauces, and drinks, and offer smart bundles that increase check size, using contextual prompts rather than intrusive pop-ups that overwhelm or slow guests.

3. Accessibility & inclusivity:

Ensure devices support large text, screen brightness, and language options where possible. Staff should be trained to assist respectfully.

Implementation Roadmap (30/60/90 Days)

1. Day 0-30 – Foundations:

Shortlist three processors or POS and run an RFP. Choose hardware mix like counter, handhelds, QR/kiosk, online ordering then order devices, map Wi-Fi, place POS on a secure VLAN.

Configure menu like modifiers, combos, taxes, service charges, define tip flows by role, enable E2EE or P2PE, set roles, enforce MFA, connect ordering or marketplaces, and dry-run batching, funding, and daily close.

2. Day 31-60 – Go-Live and Hardening:

Train staff on handheld etiquette, splits, refunds, and ID checks. Launch QR in one section, expand after 1-2 weeks. Turn on SMS or email receipts with review links, set a chargeback playbook or owner, and connect accounting; validate month-end close.

3. Day 61 – 90 – Optimize:

Monitor approvals, average tip, table turns, and fees; optimize prompts and upsells, launch gift cards and loyalty, promote them consistently, and revisit processor pricing as your volume grows.

Processor/POS RFP Checklist

1. Pricing & Contracts:

Specify interchange-plus or flat rate, exact markup, Amex or Discover treatment, all monthly or annual fees, ETF or equipment return terms, and funding speed or policy. Request a sample monthly statement using your volume or mix to model true effective rate.

2. Hardware and Reliability:

Confirm device lineup like counter, PIN pad, handheld, pay-at-table, kiosk, offline mode behavior and risk scoring, remote management like updates, battery health, swap or repair SLAs, and Wi-Fi, Ethernet, LTE guidance.

3. Software & Features:

Validate POS modules you need like table management, tabs, KDS/kitchen routing, inventory, labor, tip flows/pooling, auto-gratuity, service charges, and native online ordering with branded checkout and saved cards.

4. Security & Compliance:

Require end-to-end encryption (P2PE/E2EE), tokenization (network tokens for cards on file), your PCI scope and SAQ type, role-based access with audit logs, and signed webhooks.

5. Integrations & Data:

Ensure accounting exports (QuickBooks/Xero), payroll/tip reports, open APIs, webhooks, idempotency keys, log retention controls, and data portability if you churn.

6. Support & Operations:

24/7 support with restaurant expertise, go-live coverage, training materials, and on-site vs. advanced-exchange policies. Confirm escalation paths and response SLAs for outages, device loss, or chargeback spikes.

Conclusion:

Restaurant credit card processing is not just about rates rather it’s the backbone of service. When payments are fast, safe, and transparent, then the tables turn quicker, tips grow, and your guests leave happier.

Start with speed with tap to pay, EMV or contactless, server handhelds, and pre-authorization tabs. Pair those devices with clear, respectful tipping, and digital receipts.

Behind the scenes, reduce risk and scope with hosted or embedded fields online, P2PE or E2EE in-person, immediate tokenization, least-privilege access, short retention, and regular SAQs, and staff training.

Treat data as an asset with clean inputs, network tokens for cards on file, and smart idempotent retries which raise approvals without double charges. Operational disciplines like Z-reads and batch reports, processor deposit reconciliation, tip and payroll exports, and an account bridge to QuickBooks.

Be prepared for exceptions with a chargeback playbook, device loss steps, and signed webhooks and structured logs for traceability.Use an apples-to-apples RFP to compare vendors, and renegotiate pricing as your volume and mix evolve.

Keep iterating by tracking approval rates, average tips, table turns, and net fees, then tuning prompts and upsells and introducing loyalty and gift cards. When executed well, payments shift from a cost center to a guest-experience engine which will be a lasting competitive advantage for your restaurant which is a real processing win.