In this digital economy, businesses that are able to accept online and card payments are crucial for business success. A merchant account is the center of this functionality that enables businesses to process transactions securely and efficiently.

However, before businesses start accepting payments, it is essential for them to go through the merchant account approval process which is a detailed verification done by payment processors and acquiring banks.

The merchant account approval process verifies the credibility, financial stability, and risks of businesses. It is essential for payment providers which are essential to ensure that businesses can handle their payment transactions responsibly while reducing fraud, disputes, and chargebacks.

Many factors such as creditworthiness, business model, industry risk, and financial history are crucial for determining whether their application for a merchant account gets approved.

For many businesses such as startups and small enterprises, understanding the merchant account underwriting process may feel complex.

Whether it is submitting documentation, verifying your identity, risk assessments, and compliance checks, every step is crucial. If any details are missed or any inconsistency can lead to delays or rejection.

Through this blog, we will walk you through the merchant account approval process step by step, that helps to understand what payment providers look for and how businesses can improve their chances of approval.

Whether businesses are applying for the merchant account for the first time or willing to overcome earlier challenges then it is essential to have a clear understanding of payment processing approval, risk evaluation, and merchant account requirements that gives them an advantage to secure account approval quickly and efficiently.

Also Read: Top Merchant Account Providers Compared to Businesses

What Is a Merchant Account?

A merchant account is a specialized bank account. Such bank accounts enable businesses to process electronic payments like credit cards, debit cards, and online transactions.

This account works as an intermediary between the customer’s bank and the business’s bank which ensures that the payments are handled securely and efficiently.

Without a merchant account, businesses would struggle to accept payment solutions and grow effectively.

When a customer makes a payment, the process works as follows:

- The transaction is first authorized by the customer’s bank

- On a temporary basis, funds are held in the merchant account

- The amount is then settled and transferred to the business bank account

This system ensures:

- Secure payment processing

- Fraud detection and prevention

- Compliance with financial regulations

Also Read: Merchant Account Services Complete Guide

Why the Approval Process Matters

The merchant account approval process is essential as it protects both payment providers and the financial system. Every transaction has risks so providers must ensure that businesses that use their systems are reliable and capable of handling payments efficiently. Without proper screening, issues like fraud, more chargebacks, or financial instability may cause losses.

For example, risks can include:

- A customer disputing a transaction (chargeback)

- Fraudulent or unauthorized payments

- A business failing and being unable to issue refunds

To reduce such risks, payment providers must carefully evaluate each merchant account application before granting them access to their processing.

For businesses, the outcome of this process has a direct impact on operations:

- Determines whether you can accept card and online payments

- Affects how quickly funds are settled into your account

- Influences fees, limits, and account conditions

With a smooth and successful approval process, businesses can speed growth and improve cash flow, while delays or rejects can impact sales and obstruct business expansion.

Also Read: How Small Businesses Can Get Approved for Merchant Account

Types of Merchant Accounts

Understanding the type of merchant account you require can influence your approval process.

1. Aggregated Merchant Accounts

Aggregated merchant accounts are shared payment solutions offered by payment service providers, where multiple businesses operate under a single master account.

Rather than having a dedicated merchant account, your transactions are processed collectively, and the provider takes responsibility for compliance, underwriting, and risk management. It makes the onboarding process much simpler and faster compared to traditional merchant accounts.

Features:

- Quick setup with fast approval, often within minutes or hours

- Minimal documentation required, reducing paperwork hassles

- Lower entry barrier, making it accessible for new businesses

These accounts are good options for businesses that want to start accepting payments instantly without dealing with complex approval processes. These accounts are mostly used by startups and small businesses that may not qualify for a dedicated merchant account.

Best for:

- Startups entering the market

- Small businesses with limited transaction volume

- Low-risk operations with predictable payment behavior

Though convenient, businesses should be aware of possible limitations such as fund holds or account restrictions because of shared risk.

Also Read: What Are Merchant Services and How Do They Work For Businesses

2. Dedicated Merchant Accounts

Dedicated merchant accounts are individual payment processing accounts assigned exclusively to a single business. Unlike shared accounts, these accounts provide full ownership and control over transactions, that allows businesses to operate with greater flexibility and stability.

They are usually offered by acquiring banks or specialized payment processors after a detailed underwriting process.

Features:

- Greater control over transactions, chargebacks, and account settings

- Custom pricing models based on business volume and risk profile

- Higher approval requirements, that includes detailed documentation and credit checks

These accounts are good options for businesses that have expanded beyond the startup phase and require a reliable, scalable payment solution. Though the approval process is more rigorous and may take more time, the benefits of such accounts may outweigh the effort for established businesses.

Best for:

- Established businesses with a proven track record

- Companies handling high transaction volumes

- Businesses needing stable and customizable payment processing

Though the setup for dedicated accounts is more complex, dedicated accounts provide long-term reliability and better financial control.

3. High-Risk Merchant Accounts

High-risk merchant accounts are specialized payment processing solutions for businesses that are operating in industries that are considered risky by traditional providers.

Such risks may arise because of high chargeback rates, regulatory complexity, or unpredictable transaction patterns. Businesses in high-risk sectors must go through a detailed and cautious approval process.

Features:

- Higher processing fees to offset increased financial risk

- Additional safeguards such as rolling reserves or transaction limits

- More detailed underwriting, including thorough business and financial checks

These accounts ensure that high-risk businesses can still accept payments that offer security for payment processors. Though the costs and requirements are higher, these accounts offer access to crucial payment infrastructure which might otherwise be unavailable.

Best for:

- Subscription-based services with recurring billing models

- Travel businesses with advance bookings and cancellations

- Forex trading or cryptocurrency platforms with volatile transactions

Despite stricter conditions, high-risk merchant accounts enable business continuity and global payment acceptance.

Also Read: Why Business Get Rejected for Online Merchant Accounts

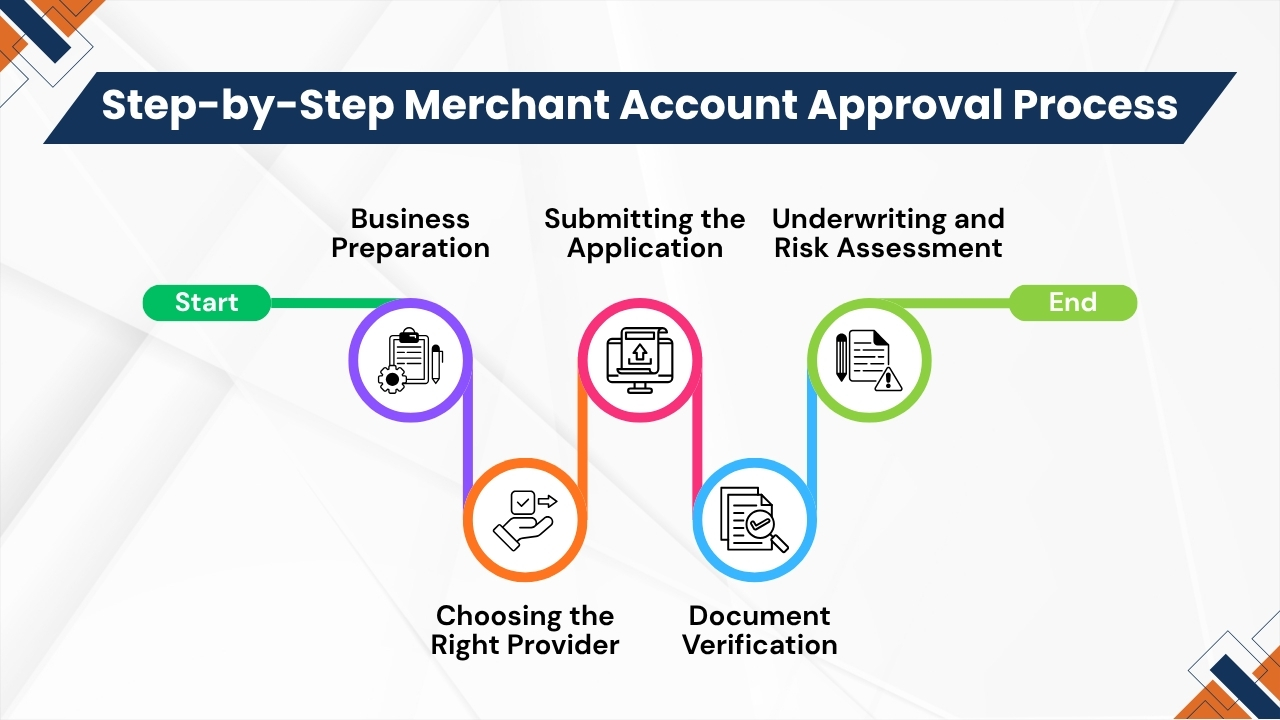

Step-by-Step Merchant Account Approval Process

Step 1: Business Preparation

Before applying for a merchant account, it is crucial to ensure that business is properly established and compliant with legal and financial requirements.

Payment providers closely evaluate to what extent your business is organized and transparent as it directly impacts their risk assessment. Proper preparation improves your chances of account approval and also speeds up the complete onboarding process.

If a business is well-structured then it indicates credibility and professionalism. And when your operations, documentation, and financial details are clear, then underwriters can easily verify your legitimacy.

It reduces communication, delays, and lowers the chances of rejection or additional analysis.

You’ll need:

- Legal business registration (such as a company, LLP, or sole proprietorship)

- A valid tax identification number (e.g., PAN and GST registration)

- A clearly defined business model outlining your products, services, and target market

Additionally, having a basic online presence, proper contact details, and organized financial records may further improve your chances of account approval. Overall, a thorough preparation helps to build trust with payment and ensures a smoother, faster approval experience.

Also Read: How to Manage Small Business Efficiently Using Modern Payment

Step 2: Choosing the Right Provider

Selecting the right merchant account provider is an important step in the approval process. Every provider does not operate the same way, instead some focus on low-risk businesses with simple requirements, while other providers specialize in high-risk industries which require more flexible underwriting.

Selecting a provider which aligns with your business type can highly improve the chances of businesses to get approved and ensures smoother payment operations.

A well-aligned provider will understand your industry, transaction patterns, and potential risks. This reduces unnecessary complications during underwriting and helps to secure better terms. However, making the wrong provider choice, can cause higher fees, delays, or even rejection.

When selecting a provider, consider:

- Pricing structure, including transaction fees, setup costs, and hidden charges

- Integration capabilities with your website, app, or existing systems

- Industry expertise and experience handling businesses similar to yours

- Customer support quality for resolving issues quickly

When businesses take the time to compare providers and evaluate these factors may make a huge difference. The right provider not just increases approval chances but also supports your business growth with reliable and efficient payment processing.

Also Read: How to Choose the Right POS For Your Business

Step 3: Submitting the Application

Submitting your merchant account application is crucial because it is the first impression that your business makes on the payment provider.

At this phase, it is crucial for businesses to be accurate and complete. Providers will depend mostly on the information that businesses submit to evaluate their credibility, risk level, and eligibility. Any missing or inconsistent details may cause additional verification checks or even rejection.

While a well-prepared application of businesses indicates professionalism and helps to establish trust with underwriters. It also speeds up the approval process by reducing follow-ups or clarifications.

Taking the time to review your application helps businesses before submission to avoid unnecessary delays.

The application typically includes:

- Business details, such as name, address, and legal structure

- Ownership information, including details of directors or partners

- Banking details for settlements and verification

- Processing history, if you have previously accepted payments

Ensure that all mentioned information aligns with your official documents and records. Even small discrepancies like mismatched addresses can increase warnings.

Having a clear and transparent application highly improves your chances of instant and successful approval.

Step 4: Document Verification

Once when a merchant account application is submitted, the provider moves to the documentation verification phase. This step is essential for confirming the authenticity of your business and ensuring it complies with legal and financial regulations.

Providers must carefully review all submitted documents to evaluate risk and validate the information provided in your application.

A smooth verification process will depend on the accuracy, clarity, and how complete your documents are. Any missing or unclear information may cause delays or additional requirements for clarification. This phase is crucial for building trust between business and the payment processor.

Common requirements include:

- Government-issued ID of business owners or directors for identity verification

- Business license or registration certificate to confirm legal existence

- Recent bank statements to evaluate financial stability and transaction history

- Proof of address for both business and owners

- Website link or detailed business plan explaining operations and revenue model

By ensuring that all documents are up-to-date and consistent with your application details, helps to streamline approval and increases the chances of a successful outcome.

Step 5: Underwriting and Risk Assessment

Underwriting and risk assessment is the most important step in the merchant account approval process. During this phase, the provider does a detailed evaluation of your business to find the financial risk involved in approving your account.

It ensures that the payment processor is protected against fraud, chargebacks, and regulatory issues.

Underwriters will analyze many aspects of your business such as industry type, transaction behavior, financial stability, and business model.

They also review your documents, website, and processing history to know how your business operates in the real-world. Based on this assessment, these providers may decide whether to approve your application, request more information, or decline it.

Providers evaluate multiple factors such as:

- Industry risk level (low-risk vs high-risk business categories)

- Expected transaction volume and average ticket size

- Chargeback ratio and refund history (if available)

- Financial stability through bank statements and credit profile

- Website quality, transparency, and compliance with policies

A strong underwriting profile increases the chances of account approval but may also result in better pricing and fewer restrictions.

Also Read: High-Risk Merchant Account Instant Approval

Key Factors Evaluated During Underwriting

Underwriting is a detailed risk evaluation process where payment providers assess whether your business is trustworthy, stable, and compliant enough for a merchant account approval.

Each factor helps to determine the level of risk involved in supporting your payment processing. Below are the six most crucial factors explained clearly:

1. Business Legitimacy

The first step for providers is to verify that your business is genuine and legally registered. Then providers may review documents, licenses, and tax identification details for ensuring authenticity.

These providers also evaluate your website, and social media presence. Having a professional website with clear product or service descriptions helps to build credibility. Transparency and clarity in your offerings increase trust and help speed up the approval process.

2. Financial Stability

Your financial health is a crucial factor for determining whether your businesses can handle transactions responsibly. Providers analyze bank statements, revenue patterns, and overall cash flow.

If there are consistent and predictable income patterns may indicate lower risk, while if there are irregular or unstable finances may lead to additional analysis. Businesses with stable growth and good financial management have high chances to receive favorable approval terms.

3. Creditworthiness

Creditworthiness shows how reliably financial responsibilities have been managed in the past. Providers may verify personal and business credit scores.

A strong credit history indicates responsibility and reduces perceived risk, which improves your chances of quick merchant account approval. A lower credit score may still be accepted but often result in stricter terms like higher fees or reserve requirements.

4. Chargeback Potential

Chargebacks are a crucial concern as it directly impacts financial risk. Providers may verify your refund policies, customer support quality, and any history of disputes.

Businesses that have unclear policies or weak support systems are more likely to face chargebacks. While high-risk profiles may have rolling reserves where funds are temporarily held to neutralize any losses.

5. Compliance and Security

Compliance along with regulations is essential for merchant account approval. And providers ensure that your business meets KYC(Know Your Customer), AML(Anti-Money Laundering), and PCI DSS standards.

These measures help to verify identity, avoid any illegal activity, and protect customer data. Having strong compliance and security practices indicates reliability and highly improve your chances of approval

Also Read: Online Transaction Security Payment Processing in Ecommerce

Approval Outcomes

After the underwriting and risk assessment is completed, the payment provider makes a final decision of your merchant account application. The outcome will depend on how well your business meets their risk, compliance, and financial requirements.

There are usually three possible results: full approval, conditional approval, or rejection. Each outcome determines how you will be able to process payments and under what terms. Understanding these outcomes helps businesses prepare better and set realistic expectations during the application process.

1. Full Approval

In this outcome, your business is approved without restrictions, and you can start processing payments immediately. Standard fees and terms apply, and there are usually no additional conditions. It is the ideal result for low-risk and well-prepared businesses.

2. Conditional Approval

In this case, your application is approved but with certain restrictions. It may include rolling reserves, processing limits, or higher transaction fees. Providers use these conditions to reduce financial risk while still allowing your business to operate.

3. Rejection

If your business is considered to be too risky or lacks sufficient documentation, that your application may be declined. It usually happens due to high-risk industries, incomplete information, or compliance issues.

Also Read: How Small Businesses Can Get Approved for a Merchant Account

Timeline for Approval

Timeline for merchant account approval depends on many factors such as the nature of your business, its risk level, and the completeness of the submitted application.

Providers evaluate each application differently based on the complexity of your operations, and how much verification is required. Generally if the business is more straightforward and well-documented then faster becomes the approval process.

Approval timelines by business type:

- Low-risk businesses: Approval can happen on the same day or 48 hours as they require less verification

- Moderate-risk businesses: Approval can take 2–7 days, due to additional financial and operational checks

- High-risk businesses: Approval can take 1–3 weeks, because of detailed underwriting and compliance reviews

Delays in account approval usually happen when documentation is incomplete, inconsistent, or requires further clarification from the provider. Ensuring accurate and properly organized information can help to highly reduce processing time and speed up approval.

How to Improve Your Approval Chances

Getting approved for a merchant account is not just about submitting an application. Instead it’s about presenting your business as trustworthy, steady, and low-risk.

Payment providers carefully check every detail, because taking proactive steps can highly improve chances of approval. With proper preparation, transparency, and professionalism all play an important role in making your application have an advantage during underwriting.

A strong application reduces delays, communication, and helps providers to feel confident in your business. Below are the most effective ways to increase your approval success rate.

1. Prepare Documentation in Advance

When businesses prepare their documentation well in advance, it makes the application process smooth and reduces the risk of delays. Ensure that all crucial documents such as business registration certificates, tax IDs, bank statements, and valid identity proof are accurate and up to date.

When businesses organize their documents indicates professionalism and improves your chances of instant approval.

2. Maintain Strong Financial Records

Maintaining strong financial records shows your business’s stability and credibility. By keeping accurate and organized accounts ensures that bank statements show consistent cash flow.

Avoid any unexplained or irregular transactions which could increase warnings during underwriting. Clear financial transparency reassures providers and highly improves your chances of quick and smooth approval.

3. Build a Professional Website

Building a professional website establishes a strong first impression and builds trust with payment providers. Also include clear product or service descriptions, accurate contact details, and essential policies such as privacy, refund, and cancellation terms.

Having a well-structured, transparent website shows legitimacy and reassures underwriters about your business credibility and compliance.

4. Be Honest and Transparent

It is essential for businesses to be honest and transparent during the application process. Always offer accurate details regarding the business model, expected revenue, and transaction volumes.

Any misrepresentation or false information can result in instant rejection or even account termination later, which damages your credibility and makes it harder to secure approvals in the future.

5. Reduce Risk Factors

Reducing risk factors increases your approval chances. It is essential for businesses to focus on delivering reliable customer support, resolving issues instantly, and handling refunds efficiently.

Maintain a high product or service quality to meet customer expectations. Such practices reduce chargebacks and disputes showing operational stability and building trust with payment providers during the underwriting evaluation process.

6. Choose the Right Provider

Choosing the right payment provider is essential for account approval success. All providers do not support every business type of risk level, so it is essential to select a provider that aligns with your industry.

A suitable provider must understand your requirements, increase approval chances, and ensure smoother operations, better support, and more reliable long-term payment processing for your business.

Conclusion

The merchant account approval process is a structured but crucial journey which ensures businesses are capable of handling electronic payments securely and responsibly.

From the initial application to the final underwriting decision, every step evaluates the legitimacy, financial stability, and risks of a business.

Though the process of merchant account approval process may seem complex, it ultimately protects payment providers and merchants by ensuring safe and compliant transactions.

A successful merchant account approval depends highly on preparation, transparency, and selecting the right provider. Businesses that maintain accurate documentation, strong financial records, and a professional online presence have far more chances to experience a smooth and fast approval process.

While incomplete applications, unclear business models, or high-risk indicators may cause delays or rejection.

It is also crucial to understand that every merchant account is not the same. From aggregated accounts for startups, a dedicated account for established businesses, or a high-risk account for specialized industries, selecting the right merchant account type plays an important role in long-term success.

Ultimately, the approval process is a safeguard which builds trust in the global payment ecosystem. By understanding each phase and preparing strategically, businesses can improve their approval chances and ensure smooth, secure, and scalable payment operations for future growth.

If you still have any query about the merchant account approval process then you may book a free demo at Ace Merchant Processing and we are more than happy to assist you.