Choosing the best merchant account provider is one of the most important decisions that a business can make while setting up a dependable and profitable payment processing system.

In this highly competitive market, businesses require beyond a basic way to accept credit card payments and debit card payments.

Businesses require a complete merchant services provider which offers secure transactions, transparent pricing, fast funding, strong customer support, and the flexibility to handle both in-store payments and online payments.

So if you are running a startup, ecommerce brand, retail store, restaurant, service business, or enterprise operation, the right merchant account services can directly impact cash flow, customer experience, and long-term growth.

A reliable provider helps businesses to process payments smoothly, reduce transaction friction, manage chargebacks, improve checkout speed, and support multiple payment methods such as mobile payments, ACH payments, recurring billing, invoices, and point-of-sale systems.

While, the wrong provider can cause hidden fees, weak support, slow deposits, and a payment setup that does not scale with your business.

That is why comparing the top merchant account providers is essential. Not every business requires the same merchant account provider solution.

Some companies prioritize low fees, while other companies require strong ecommerce payment solutions, advanced integrations, payment gateway support, or industry-specific tools.

The ideal choice depends on your business model, monthly processing volume, risk profile, and customer payment preferences.

Through this blog, we will compare the top merchant account providers for businesses, review their strengths, pricing models, features, and business fit, and help you understand which payment processor may be the best choice for your needs.

If you want to improve payment efficiency and choose the right merchant account provider, this comparison will give you a clear starting point.

Also Read: Merchant Account Service Complete Guide for Businesses

Why Merchant Account Selection Matters More Than Most Businesses Expect

Merchant account selection matters more than many businesses expect because payment systems affect far more than card acceptance.

Many businesses only realize their current payment provider no longer fits their needs when issues such as delayed funding, higher costs, weak conversion, poor POS flexibility, or poor system integration start affecting daily operations.

In many cases, payments still function, but they quietly reduce profit margins, slow operations, and create extra administrative work.

One major reason this happens is because of pricing structure. Different providers use different models, like pay-as-you-go, interchange-plus, or subscription pricing.

These structures change how predictable costs feel, how transparent statements are, and whether the pricing works best for low, seasonal, or high processing volume. A provider which may look affordable initially may become less efficient as the business grows.

Workflow fit is another essential factor. A payment provider must match how the business actually operates. Retail stores, service businesses, ecommerce brands, and multi-location companies all have different requirements, so the same provider will not fit every model equally well.

Support is equally important. Businesses often focus on setup, but the real test comes when there are chargebacks, deposit delays, terminal issues, or billing errors. A merchant account is not a one-time decision. It is an ongoing revenue-critical relationship.

Also Read: Instant Approval Online Merchant Account

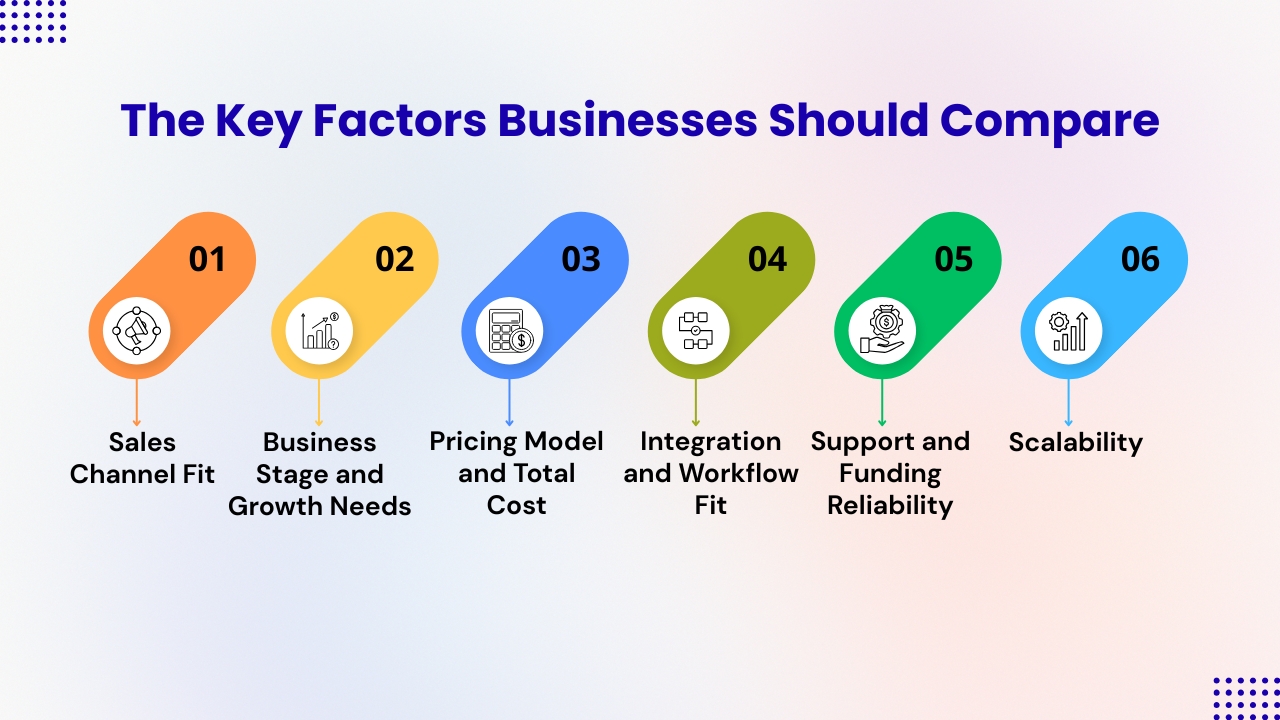

The Key Factors Businesses Should Compare

1. Sales Channel Fit

Begin by looking at how your business accepts payments. Some companies are mostly in person, while other businesses sell mainly online, send invoices, run recurring billing, or operate across multiple channels. The right merchant account provider should match the way you sell every day.

2. Business Stage and Growth Needs

A startup has very different requirements from a growing business or multi-location company. So before selecting a provider, consider whether you require simple solutions or solutions that can support long-term expansion.

3. Pricing Model and Total Cost

Businesses should not just check only on the advertised rate. Rather compare the full pricing structure that includes monthly fees, transaction markups, hardware costs, gateway fees, dispute charges, and other add-ons. So even a provider with a low rate can still be costly overall.

4. Integration and Workflow Fit

Your payment provider should work smoothly with your website, POS, CRM, ERP, and accounting tools. If integrations are weak, reporting, reconciliation, and day-to-day operations can become more difficult.

5. Support and Funding Reliability

Good support is essential when issues arise, such as chargebacks, delayed deposits, or technical problems. Businesses should also compare funding speed, account stability, and how well the provider handles risk.

6. Scalability

Choose a provider that can support your business as it grows, which includes higher transaction volume, more locations, expanded product lines, and greater operational complexity without forcing a costly switch later.

Also Read: Why Business Get Rejected for Online Merchant Account

Top Merchant Services Providers Compared for Business Growth

1. Finix: Best For Enterprise-Level Businesses

Finix is a strong choice for enterprise-level businesses because it offers more than standard payment processing. Its broader infrastructure includes ACH support, subscription billing, hosted fields, fraud tools, and Level 2 and Level 3 processing.

These features make it suitable for companies which need scalability, customization, and stronger payment control. However, smaller businesses that want simple setup, easy pricing, and basic card acceptance may find Finix more advanced than necessary for their current requirements.

Typical Pricing

Finix pricing begins at $250 per month for card processing, with 0% markup on interchange and card network fees. Card-present transactions begin at $0.08 each, card-not-present transactions at $0.15 each.

Advantages

- Strong fit for large and complex businesses.

- Supports advanced payment features and enterprise workflows.

- Good for scalability, customization, and risk management.

- Includes implementation and developer support.

Disadvantages

- Higher starting cost than many small-business providers.

- May be too complex for businesses with simple payment needs.

- Best value usually comes only when a business can fully use its advanced features.

Also Read: How to Manage Small Business Efficiently Using Modern Payment System

2. Stax: Strong for Low Fees at Higher Volume

Stax is a strong option for businesses that process higher payment volume and want more control over their processing costs. Forbes Advisor currently lists Stax for “best for low fees” with a starting monthly price of $99 plus transaction fees.

Stax uses a subscription-based pricing model and advertises 0% markup on direct-cost interchange, which makes it different from typical flat-rate processors.

Typical pricing

Stax plans begin at $99/month for up to $150,000 in annual processing, $139/month for $150,000–$250,000, and $199+/month above that.

Stax also lists $0.08 per card-present transaction, $0.15 per card-not-present transaction, and ACH processing at 1% per transaction capped at $10.

Advantages

- Transparent subscription pricing

- No percentage markup on interchange

- In-house support

- Next-business-day funding

- Tools like invoicing, recurring billing, analytics, and fraud protection

Disadvantages

- The monthly fee may not make sense for low-volume or unpredictable businesses

- The best savings usually come only when processing volume is consistently high

Also Read: What Payment Methods Should Retailers Accept

3. Helcim: Excellent for Startups and Seasonal Businesses

Helcim is a strong option for startups and seasonal businesses because it offers transparent interchange-plus pricing with no monthly fees, no PCI fees, no minimums, and no cancellation fees.

It also advertises next-business-day deposits at no extra cost, which makes it attractive for merchants that want professional payment processing without heavy fixed overhead.

Overall, Helcim works well for businesses that need flexibility, cost control, and grow without long-term fee pressure.

Typical pricing

Helcim is built around volume-based interchange-plus rates. Helcim shows in-person pricing from Interchange + 0.40% + 8¢ for lower volumes down to Interchange + 0.15% + 6¢ at higher volumes, with a sample effective in-person rate of 1.83% + 8¢ and online/keyed effective rate of 2.61% + 8¢. ACH payments are 0.5% + 25¢, capped at $6.

Advantages

- Low commitment

- Clear pricing

- No recurring monthly overhead

- Volume discounts

- Faster funding

Disadvantages

- Interchange-plus pricing of Helcim may feel less simple than flat-rate pricing

- Recurring payments add +0.4% per transaction

- Merchants wanting the easiest possible pricing model may prefer a simpler flat-rate provider

Also Read: Merchant Processing Services Explained for Small Businesses

4. Stripe: Best for Website Integration and Online Flexibility

Stripe is one of the strongest options for digital-first businesses because it is built for website integration, online payments, subscriptions, and custom checkout workflows.

Forbes Advisor currently ranks Stripe as best for website integration, and Stripe says its standard model uses pay-as-you-go pricing with no setup fees, monthly fees, or hidden fees, while larger businesses can request custom pricing.

Stripe also highlights support for more than 100 payment methods, which makes it attractive for startups, SaaS companies, marketplaces, and modern ecommerce brands.

Typical pricing

Forbes lists Stripe with a $0 starting monthly price and 2.9% +$0.30 for both tap, dip, or swipe transactions and online processing in its 2026 comparison. Stripe also notes that custom packages are available for businesses with large payment volume or unique models.

Advantages

- Flexible integrations

- Strong developer tools

- Broad payment method support

- No monthly fee

- Stronger fit for online growth

Disadvantages

- It is not always the lowest-cost option

- Some businesses may want more advisor-led support

- Simpler merchants may find traditional providers easier to manage operationally

Also Read: How to Build a Payment Franchise With Ace Merchant Processing

5. Payment Depot: Strong For Businesses that Want Custom Interchange-Plus Style Quotes

Payment Depot is a strong option for businesses that want a more customized pricing structure rather than a one-size-fits-all flat-rate model.

Forbes Advisor currently names it best for software integrations, while Payment Depot says it offers transparent interchange-plus pricing customized to each business.

Its official site also says variable rates can begin as low as 0.2% to 1.95%, depending on the merchant’s needs and profile.

Typical Pricing

Payment Depot does not publish a single fixed public pricing chart, as rates and fees are usually customized based on each business’s needs and processing profile.

Forbes notes that both monthly fees and transaction fees are customized per merchant, and Payment Depot emphasizes a quote-based approach built around business type, sales volume, and integration requirements.

As a result, businesses usually need to contact the sales team to receive accurate pricing based on their volume, industry, and payment requirements.

Advantages

- Customized interchange-plus pricing

- Strong software integration focus

- More customized fit for businesses using POS, accounting, CRM, or inventory tools

Disadvantages

- Pricing is less transparent upfront

- Comparing options can take more time, and businesses that prefer clear, instant pricing without a sales process may find providers like Helcim or Square easier to evaluate.

Also Read: Restaurant Credit Card Processing

6. PayPal: Best for Omnichannel Businesses and Checkout Familiarity

PayPal is a strong option for omnichannel businesses because it combines broad channel coverage with a brand customers already recognize.

Forbes Advisor ranks it best for omnichannel businesses that reflects PayPal’s ability to support online checkout, wallet-based payments, QR transactions, invoicing, Venmo, and standard card payments in one ecosystem. That makes it useful for businesses that want flexibility and more payment choice at checkout.

Typical pricing

PayPal Checkout and Guest Checkout are 3.49% + fixed fee, QR code transactions are 2.29% + fixed fee, Pay with Venmo is 3.49% + fixed fee, and standard credit and debit card payments are 2.99% + fixed fee. Pay by Bank (ACH) for invoicing is 1%, capped at $10 per transaction.

Advantages

- Strong brand familiarity

- Multiple payment options

- Good omnichannel flexibility

Disadvantages

- Pricing is not always the lowest

- Fee structures vary by payment type

- Businesses may need to compare carefully understand total cost

Also Read: Top 5 Features Every Retailers Should Look into a Modern Payment Terminal

7. Shopify: Best For Ecommerce-First Businesses

Shopify is a strong choice for ecommerce-first businesses because it combines storefront management, checkout, payments, inventory, analytics, multiple sales channels, and POS tools in one system.

Forbes Advisor ranks Shopify as best for ecommerce, which reflects how well it fits businesses that want commerce and payments to work together in a single platform. This all-in-one approach can reduce complexity and make daily operations easier for online brands.

Typical Pricing

Shopify’s India pricing starts at ₹1,499/month for Basic, ₹5,599/month for Grow, ₹22,680/month for Advanced, and ₹1,75,000/month for Plus on yearly billing. Shopify also lists third-party payment provider fees starting at 2%, 1%, and 0.6% depending on plan.

Advantages

- All-in-one ecommerce ecosystem

- Integrated checkout and POS

- Strong analytics

- Multi-channel selling tools

Disadvantages

- It works best when your business already runs on Shopify

- Costs can rise with higher-tier plans or added apps

Also Read: Smart Payment Solutions for Gaming and Esports

8. Payline Data: Worth Considering For High-Risk And Flexible Payment Needs

Payline Data is a practical option for businesses that need flexibility across payment channels or risk profiles. Forbes currently places Payline in the high-risk category, while Payline positions itself around in-person, online, recurring, and high-risk processing with transparent pricing and support.

It offers a practical balance between basic startup payment tools and complex enterprise platforms, making it suitable for a wider range of businesses.

Typical Pricing

Forbes 2026 roundup lists Payline at $10 per month with interchange + 0.4% + $0.10 for in-person payments and interchange + 0.75% + $0.20 for online payments. Another Forbes pricing roundup lists Payline at $10 per month plus 0.20% + $0.10 per transaction, which suggests pricing can vary by plan or use case.

Advantages

- Strong fit for higher-risk merchants

- Recurring billing support

- Transparent pricing language

- Next-day funding at no extra charge

Disadvantages

- Pricing is not as simple as flat-rate models

- Exact costs may vary depending on business type and processing setup

Also Read: High-Risk Merchant Account Instant Approval

9. QuickBooks Payments: Best for Service Providers and Accounting-Led Workflows

QuickBooks Payments is a good solution for service providers because it connects payments, invoicing, recurring billing, in-person acceptance, and accounting workflows in one system.

Forbes Advisor currently ranks quickbooks payments as best for service providers, that makes sense for businesses relying on estimates, invoices, bookkeeping, and client billing instead of retail-style checkout.

Typical pricing

QuickBooks lists 2.99% for cards and digital wallets paid through invoices or recurring payments, 1% for ACH bank payments, 2.5% for in-person payments, and 3.5% for keyed-in cards. It also says there are no setup costs or hidden fees, and merchants processing over $2,500 per month may qualify for discounted rates.

Advantages

- Strong accounting integration

- Invoice-first workflow support

- Recurring billing

- Mobile and in-person payment options

- Fast deposit tools

Disadvantages

It is less focused on advanced ecommerce customization

Businesses outside the QuickBooks ecosystem may get less value from its accounting-led setup.

Also Read: How to Choose the Best Service Merchant Providers

10. Chase Payment Solutions: Best for Businesses That Want a Bank-Backed Relationship

Chase Payment Solutions is a strong option for businesses that want merchant services backed by major banks. Forbes Advisor currently ranks it best trusted financial institution.

It promotes support for in-person payments, website gateways, billing and invoicing, recurring billing, mobile acceptance, and ecommerce integrations.

It uses a more consultative model that encourages businesses to connect with a payment advisor for customized product recommendations and pricing details.

Typical pricing

Chase lists 2.6% + 10¢ for tap, dip, or swipe transactions, 3.5% + 10¢ for manually keyed transactions or payment links, and 2.9% + 25¢ for ecommerce transactions. Chase also notes that monthly fees may apply to certain products and pricing plans, while some tools such as the ecommerce gateway or virtual terminal start from $9.95 per month.

Advantages

- Bank-backed credibility

- Broad payment-channel support

- Advisor-led setup

- Clear fee visibility

Disadvantages

- Less instant and lightweight than some competitors

- Possible monthly fees

- Setup style that may feel slower for businesses requiring pure self-service

Also Read: Payment Gateway Vs Payment Processor

11. Square: One of The Best Choices for in-Person Simplicity

Square is a strong option for businesses that want simple, easy-to-launch payment processing for in-person sales. Its pricing page reveals the platform costs starts at $0 and has no hidden fees or locked-in contracts that makes it attractive for retailers, service businesses, pop-ups, and local stores that require a straightforward setup.

Typical Pricing

Square lists 2.6% + 15¢ for in-person tap, dip, or swipe payments, 2.9% + 30¢ for online API payments, 1% with a $1 minimum for ACH invoice transfers, and 3.5% + 15¢ for manually entered cards or card-on-file payments.

Advantages

- Simple onboarding

- Transparent pricing

- No long-term contract

- All-in-one setup that combines payments with software and hardware tools

Disadvantages

- It may not be the most cost-efficient option for very high-volume merchants

- Businesses with highly customized payment requirements may outgrow its simpler structure.

Also Read: How to Choose the Right POS System for Your Business

12. Ace Merchant Processing: Flexible Merchant Services for Growing Businesses

Ace Merchant Processing is positioned as a brand merchant-services provider for businesses that require payment acceptance, POS tools, gateway access, and industry-specific support in one place.

Its site highlights in-person, online, and mobile payments, along with EMV terminals, POS systems, the Vaultix Gateway, gift and loyalty tools, and merchant cash advance options.

Ace also emphasizes support for a lot of industries that include retail, restaurants, healthcare, professional services, hospitality, contractors, nonprofits, and CBD businesses.

The company promotes fast setup, real-time insights, built-in fraud defense, recurring billing, and 24/7 support.

Typical pricing

Ace does not publish transaction-rate pricing on its homepage, but it clearly promotes $0 setup or hidden fees and 100% transparent pricing. It also claims 99.9% uptime, 24/7 real support, and $2 billion+ processed annually.

Advantages

- Wide solution range

- Strong industry coverage

- Transparent-fee messaging

- Recurring billing support

- Real-time reporting

- Around-the-clock support

Which Provider is Best for Which Type of Business?

1. Startups, Side Businesses, and Seasonal Merchants

Helcim is one of the best choices for businesses that require low fixed overhead and transparent pricing without monthly, PCI, or hidden fees.

Stripe can also work well for digital startups, but Helcim is often a better solution when low commitment matters more than developer flexibility. Square is an excellent option for simple in-person selling which offers speed, usability, and quick setup.

2. Ecommerce-First Brands

Shopify and Stripe are usually the most logical comparison for online businesses. Shopify is an excellent option when the store already runs on Shopify and the business requires payments connected to checkout, inventory, analytics, and sales channels.

Stripe is an excellent option for companies that need broader payment infrastructure for websites, apps, subscriptions, marketplaces, or custom online experiences. PayPal is also useful when checkout familiarity and payment choice matter.

3. Service Businesses and Larger Merchants

QuickBooks Payments is ideal for businesses built around invoicing and accounting workflows, while Ace Merchant Solutions is better for flexible cards, ACH, recurring billing, one-time invoices, and hands-on support. For higher-volume merchants,

Stax, Finix, and Payment Depot become more relevant depending on volume and complexity. Chase suits businesses wanting a bank-backed relationship, while Payline Data and Ace Merchant Solutions are valuable for specialized or harder-to-place industries.

Conclusion

Choosing the right merchant account provider is not just about finding the lowest rate or implementing the well known provider. Rather it is about selecting a payment partner that matches your business model, supports your operations, and helps your business to grow without any unnecessary cost or expenses.

Payment processing affects much more than transactions. It influences cash flow, customer experience, reporting accuracy, operational efficiency, funding speed, and how easily your business can scale over time.

That is why it is essential for businesses to compare providers based on more than just pricing. The best decision comes from looking at pricing structure, total cost, integrations, support quality, payment flexibility, funding reliability, and long-term scalability.

A provider that works well for a startup may not be the best fit for a larger enterprise, and a platform designed for ecommerce may not serve a service business or in-person retailer equally well.

Each provider brings different strengths. Helcim is strong for startups and seasonal businesses, Stripe and Shopify are excellent for digital and ecommerce-first companies, QuickBooks Payments fits invoice-driven service businesses, and Square stands out for simple in-person selling.

Stax, Finix, and Payment Depot are better suited for businesses that need more volume-based or advanced payment solutions. Chase offers a bank-backed approach, while Ace Merchant Solutions and Payline Data provide flexibility for merchants with more specialized needs.

In the end, the best merchant account provider is the one that fits your business today and continues supporting it as your needs evolve.

If you still have any query with top merchant account providers for businesses then you may book a free demo we are more than happy to assist you.